Market Commentary

Bitcoin

New years bring new beginnings (and seasonality effects). Because tax calculations & other reporting requirements happen on an annual basis, the turn of each year typically exposes a few seasonality effects that typically impact price.

An example would be tax-loss harvesting. This is when investors sell an asset that has performed poorly during the calendar year at the end of the year, in order to book the capital loss and offset other gains in their portfolios in the same calendar year. This tax treatment may also apply to Bitcoin, and it is exactly what Michael Saylor and Microstrategy did last week.

Let’s use this example to show how it works. Microstrategy has been buying bitcoin over the last few years, and it has so far acquired ~132,500 Bitcoin at an average price of ~$30,397 per bitcoin. By selling 704 BTC at $16,761, it created a taxable loss of $9.6 Million (($30,397 - $16,761) * 704), which it can use to potentially offset previous or future capital gains. This benefit doesn’t only apply to Microstrategy, and you can be certain that other U.S. investors were also “tax harvest selling” some BTC in December.

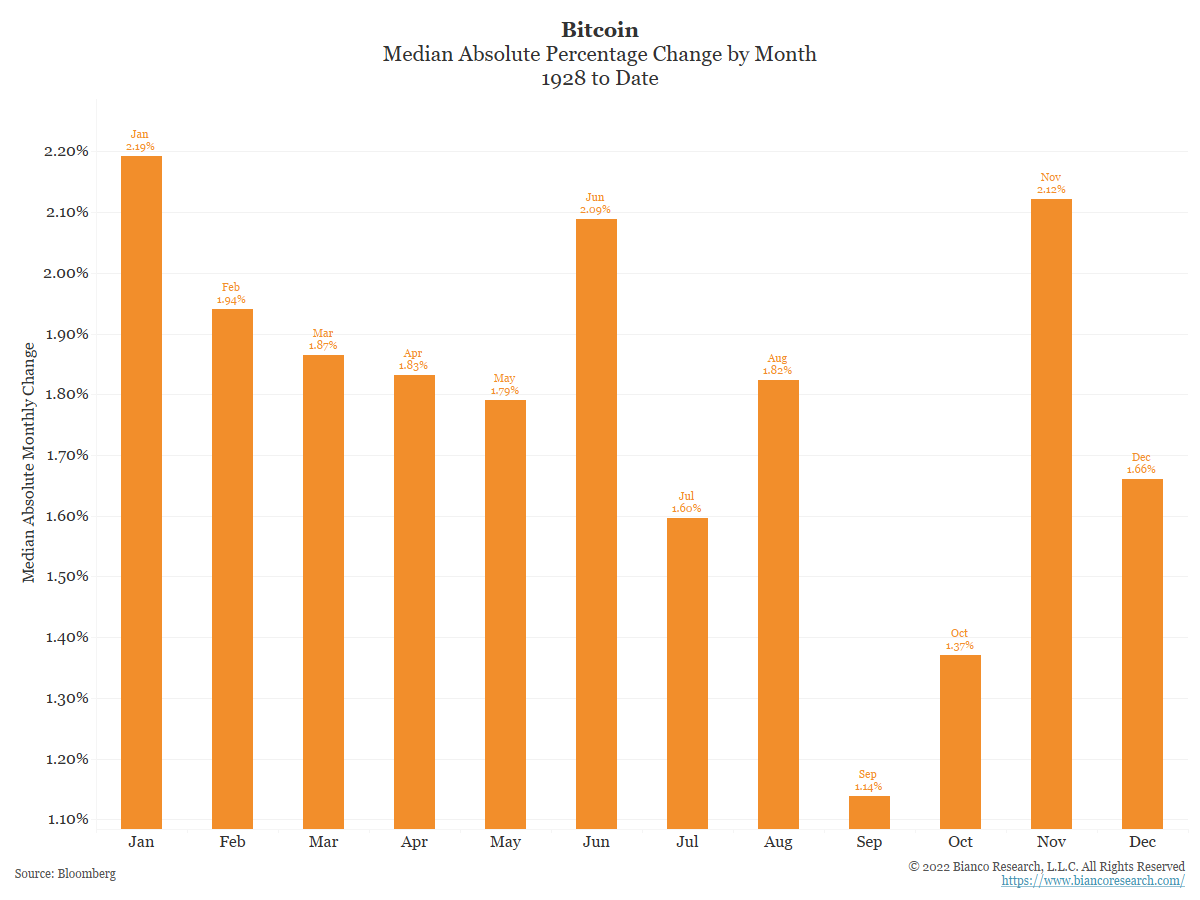

Tax harvesting is only one of the many seasonal effects in markets. Another one is calendar year seasonality. Below is a chart of Bitcoin’s historical price changes by month.

As you can see from the chart, January is the month with the biggest price changes on average. This type of seasonality could be attributed to many factors, including tax loss harvesting lags, and portfolio rebalancing at the start of each year. Regardless, January has historically been a month of big movements in bitcoin price. We also see big moves in June, which marks the 6-month mark each year, and November, which again, could be the start of tax selling season. These would be consistent with start of the year, middle of the year, and end of the year rebalancing of portfolios.

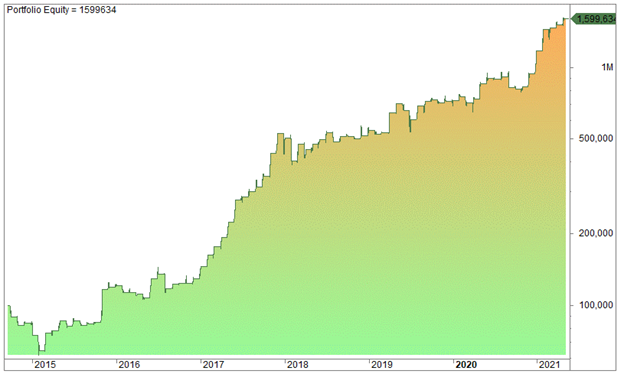

Next, we’ll look at the “turn of the month” effect. This is a trading strategy that calculates the performance of buying bitcoin on the 5th last trading day of each month, and selling it on the 3rd trading day of the new month. The graph below shows the historical progress of a bitcoin portfolio that uses this strategy.

As you can see from the chart, this strategy would have returned a compound annual growth rate of 51.3% with a maximum drawdown of -38%, meaning a return:drawdown ratio of 1.35. Comparatively, buying and holding during the same period would have yielded returns of 94.2% and a maximum drawdown of -83%, or a return:drawdown ratio of 1.13.

Potential reasoning for this turn-of-month phenomenon could be:

- The aggregate effect of monthly dollar-cost-averaging. As most people get their paychecks at the end or start of each month, the aggregate effect of thousands of small orders could provide a tailwind for bitcoin.

- At a corporate or institutional level, portfolio decisions are typically made on a monthly or quarterly basis. With so many institutions getting into bitcoin during the sample period, the aggregate effect of institutions deciding to enter positions at the start of the month or quarter, could also provide a tailwind or rationale for this phenomenon.

Seasonality aside, macroeconomic indicators still point to lower inflation and a deteriorating economy in the U.S.. The U.S. consumer’s balance sheet is quickly deteriorating, and the housing market is starting to roll over. This suggests that there could be further weakness in asset prices in general. More on this in our S&P section.

There was another event that created headlines within the bitcoin community. Luke Dash Jr., a prominent bitcoin core developer, tweeted last week that his self-custodied bitcoin hot wallet had been compromised, and over 200 BTC (USD $3.6 M) had been drained.

While the recent events surrounding the FTX fraud and bankruptcy showed that there are risks associated with using custodial services, the fact that even a bitcoin core contributor had his self-custody wallet keys compromised highlights that there is no “one-size-fits-all” solution to storing your bitcoin. People have different skills and preferences, and our industry should be focused on solutions for everybody in the spectrum. At Ledn, we encourage clients to have a diversified portfolio and learn about self custody, while also providing a suite of services, like savings accounts and loans, for those who can benefit from them.

S&P 500

Along with champagne and fireworks, the new year also brings us new analyst estimates from the top investment banks. In this week’s dispatch we’re going to review the most recent estimates and get a sense of what the top strategists in the investment world see for 2023.

The chart below shows the S&P 500 targets for the end of 2023 from the top investment banks on Wall Street.

As you can see from the chart, there is a 28% variability from the top estimate to the bottom one. Two of the biggest and most prominent banks in the U.S, Goldman Sachs and JPMorgan Chase, show their targets at 4,000 and 4,200. This is equivalent to approximately a 4-9% annual return.

Perhaps the biggest takeaway from this chart is that only one out of 24 investment banks has the S&P 500 making a new all-time high in 2023 - and only one bank shows the S&P 500 breaking the 2022 lows. In short, most investment banks expect a year of sideways trading - or a volatile ride to nowhere. Do take these with a grain of salt, as the street has a poor record of actually forecasting year-end results correctly.

In addition to S&P 500 estimates, many banks have also published year-end estimates for U.S. bond interest rates. Here is where things get more interesting - because the Federal Reserve’s forecast is public, and we can see how much they deviate - or agree with them.

Chart credit: @Macroalf

The only bank out of the 12 on the chart that’s in agreement with the Fed and sees rates higher is Goldman Sachs. Every other bank sees rates coming down considerably. Given how tight the job market in the U.S. is, it’s surprising to see Goldman be the only one in that camp.

While Q4 earnings season doesn’t kick off officially until next week, the first trading week of the year is historically the most volatile one for the S&P 500.

We’ll keep you up to date with earnings reports relevant to bitcoin in the coming weeks.

Gold

Gold’s return for 2022 was effectively zero, or -0.35% to be precise. Although that may sound underwhelming, keep in mind that 2022 was a year in which bonds and stocks were down in double digits.

As we shared in our “predictions” issue last week, we believe that the growing optimism around investors for gold should materialize into higher prices throughout 2023. In a similar vein, other gold analysts also shared optimistic price targets last week as reported by CNBC.

The calls were generally bullish, including one with one analyst who sees the prices moving north of $4,000. As a reminder of why gold prices are relevant to bitcoin, consider the following chart showing correlations between Bitcoin prices to gold and to the S&P 500.

Notice how Bitcoin has a higher correlation with gold prices than with the S&P 500 at the moment. While this has not been the norm over the last 2 years, in the long term, bitcoin should trade with a closer correlation to gold than to equity markets.

DeFi

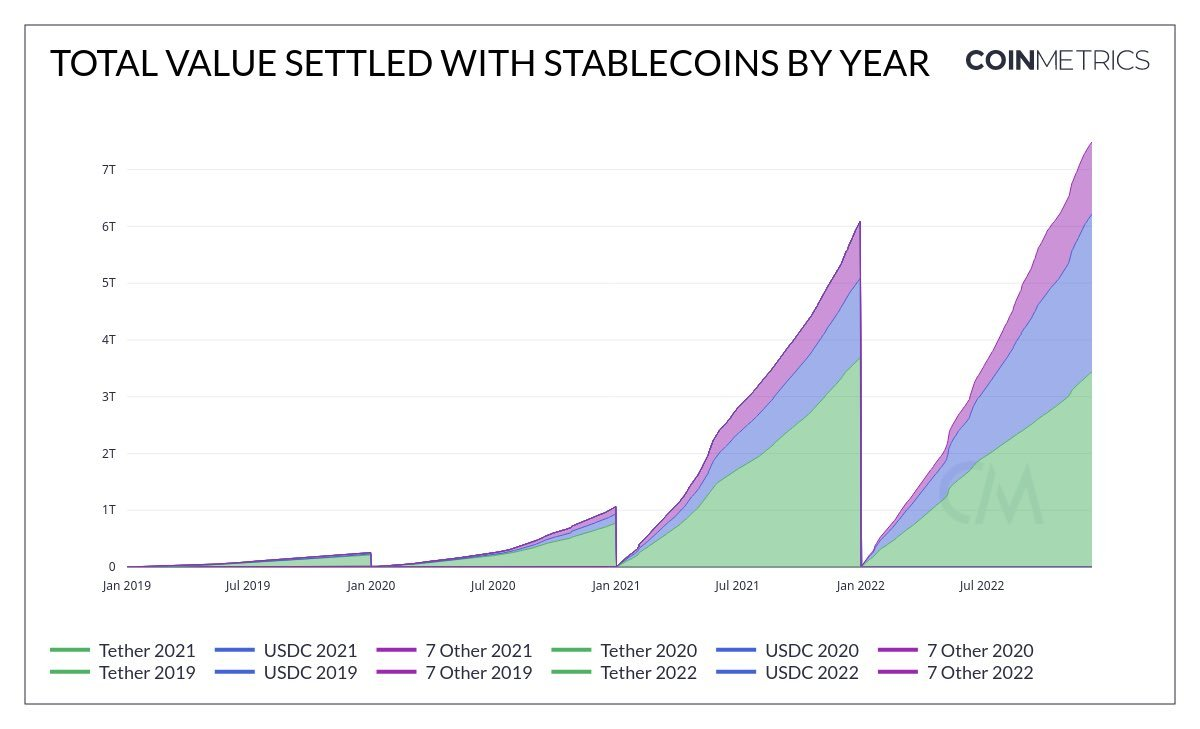

Not many charts in crypto went upwards and to the right last year - but one exception was the total value settled with stablecoins.

As per the chart above, there was more than 7 Trillion in value settled via stablecoins throughout 2022 - which is almost one trillion higher than 2021. That’s equivalent to a 14% annual increase in settled value.

For context, the SWIFT inter-bank wire transfer system facilitates about $150 Trillion per year. Meaning that stablecoins settlements equate to about 5% of the total value settled through the SWIFT system.

A quick comparison between stablecoins and wire transfers should illustrate why stablecoins will continue eating market share from SWIFT when it comes to transferring money internationally:

|

Accessibility |

Processing Time |

Cost |

|

|

Stablecoins |

24/7 |

Instant |

$1- $15 |

|

Bank Wire Transfers |

Workdays only, from 9 AM - 4 PM |

Up to 4 business days |

$25 - $50 |

Solutions that are better and more convenient to consumers eventually win over time. Given the clear benefits of transacting in stablecoins vs. using bank wire transfers, stablecoins should continue to eat away market share on settled value from the SWIFT network in the years to come.

Difficulty Commentary

As we’ve been suggesting in our last few dispatches, consolidation in the bitcoin mining space is starting to materialize. Last week Galaxy Digital announced it had acquired a Bitcoin mining facility from Argo Blockchain.

The $65 Million transaction was part of Argo’s efforts to stave off bankruptcy. Expect more of these types of news in the coming weeks or months, as well capitalized companies look to take advantage of distressed operators to purchase quality assets.

The Week Ahead

It’s the first trading week of the year and, as we covered in the S&P 500 section, this has historically been a volatile week for markets. In terms of economic data, the minutes from the Fed’s last FOMC meeting will be released on Wednesday, and markets could react to that. We already know that the Fed intends to raise rates a bit higher and keep them there for the year - but any additional detail around their collective or individual views could generate headlines.

We will also get another read at U.S. job openings, which are expected to show a slight reduction, but even at these levels - the data still shows about 2 job openings per every unemployed American. It is trending in the right direction, and given where macroeconomic indicators are, it would not be surprising to see these job openings collapse in the near future. Expect more headlines around the U.S. labour market in the near future.

In the crypto world, the Genesis restructuring talks are not going great. The pressure has been building for Gemini, as clients of their Earn product - who collectively have a claim for $900 million, started a class action lawsuit against the exchange’s founders, the Winklevoss, who are known billionaires.

The Winklevoss are now transferring that pressure over to Genesis. Yesterday Cameron Winklevoss published an open letter on Twitter addressed to Barry Silbert, CEO and founder of DCG, Genesis Capital’s parent company.

Mr. Silbert responded to the letter via a comment - to which Mr. Silbert, in the same tweet, responded that Genesis had submitted a proposal on December 29th and “had not received a response”.

The next deadline for an agreement is set for January 8th (this Sunday) - and any headline around this could move crypto markets.

As always, here’s a summary of the events and data that could move markets in the week ahead:

Wednesday

10.00 AM EST - U.S. Job Openings. Estimate is for 10.1 Million, down from last month’s 10.3 Million. This is trending in the direction that the Fed wants to see. However, even with the current reduction, there are still approximately 2 job openings for every unemployed American person. These are still extremely tight conditions, supporting the idea that the Fed must maintain interest rates higher for longer.

02.00 PM EST - FOMC Meeting minutes from December 14th meeting.

Friday

08.30 AM EST - Non-farm Payrolls (new non-farm employment in the U.S.). Expectation is for 180,000 new jobs created, down from 262,000 in November.

08.30 AM EST - U.S. Unemployment: Expectation is for unemployment to come in unchanged vs. October at 3.7%.

It's a big week coming up, and as always, we'll keep you posted on any relevant news throughout the week right here and from our Twitter account.

Notice for U.S. Residents: Effective April 4, 2022, U.S. clients will no longer be able to earn interest on any newly deposited funds in their BTC and/or USDC Savings Accounts, where available; however, they will continue to earn interest on their pre-existing balances in their BTC and/or USDC Legacy Savings Accounts.

This article is intended for general information, educational and discussion purposes only, it is not an offer, inducement or solicitation of any kind, and is not to be relied upon as constituting legal, financial, investment, tax or other professional advice. This article is not directed to, and the information contained herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to law or regulation or prohibited by any reason whatsoever or that would subject Ledn and/or its affiliates to any registration or licensing requirement. This article is expressly not for distribution or dissemination in, and no Ledn product or service is being marketed or offered to residents of, the European Union, the United Kingdom, the United States of America or any jurisdiction in Canada, and such product or service may only be marketed or offered in such jurisdictions pursuant to applicable laws or reliance on regulatory exemptions. A professional advisor should be consulted regarding your specific situation. Digital assets are highly volatile and risky, are not legal tender, and are not backed by the government. The information contained in this publication has been obtained from sources that we believe to be reliable, however we do not represent or warrant that such information is accurate or complete. Past performance and forecasts are not a reliable indicator of future performance. Any opinions or estimates expressed herein are subject to change without notice. This article may contain views or opinions of the author that do not necessarily reflect the opinions, standards or policies of Ledn. We expressly disclaim all liability and all warranties of accuracy, completeness, merchantability or fitness for a particular purpose with respect to this article/communication. Read our Disclaimers at https://ledn.io/legal/disclaimers