The U.S. dollar index breaks down - implications for bitcoin. Ethereum price is up 133% in 35 days. Understanding deflationary pressures.

Not yet a Ledn client? Start earning 12.50% APY on your USDC and 6.10% APY on your first 2 Bitcoin - click here to open your Ledn account!

Follow us on social media:

The Bitcoin Economic Calendar:

Week of Monday May 10th to Sunday May 16th.

Market Commentary:

Bitcoin: bitcoin had a contested close on Sunday evening as it finished at $58,305, +2.97% for the week.

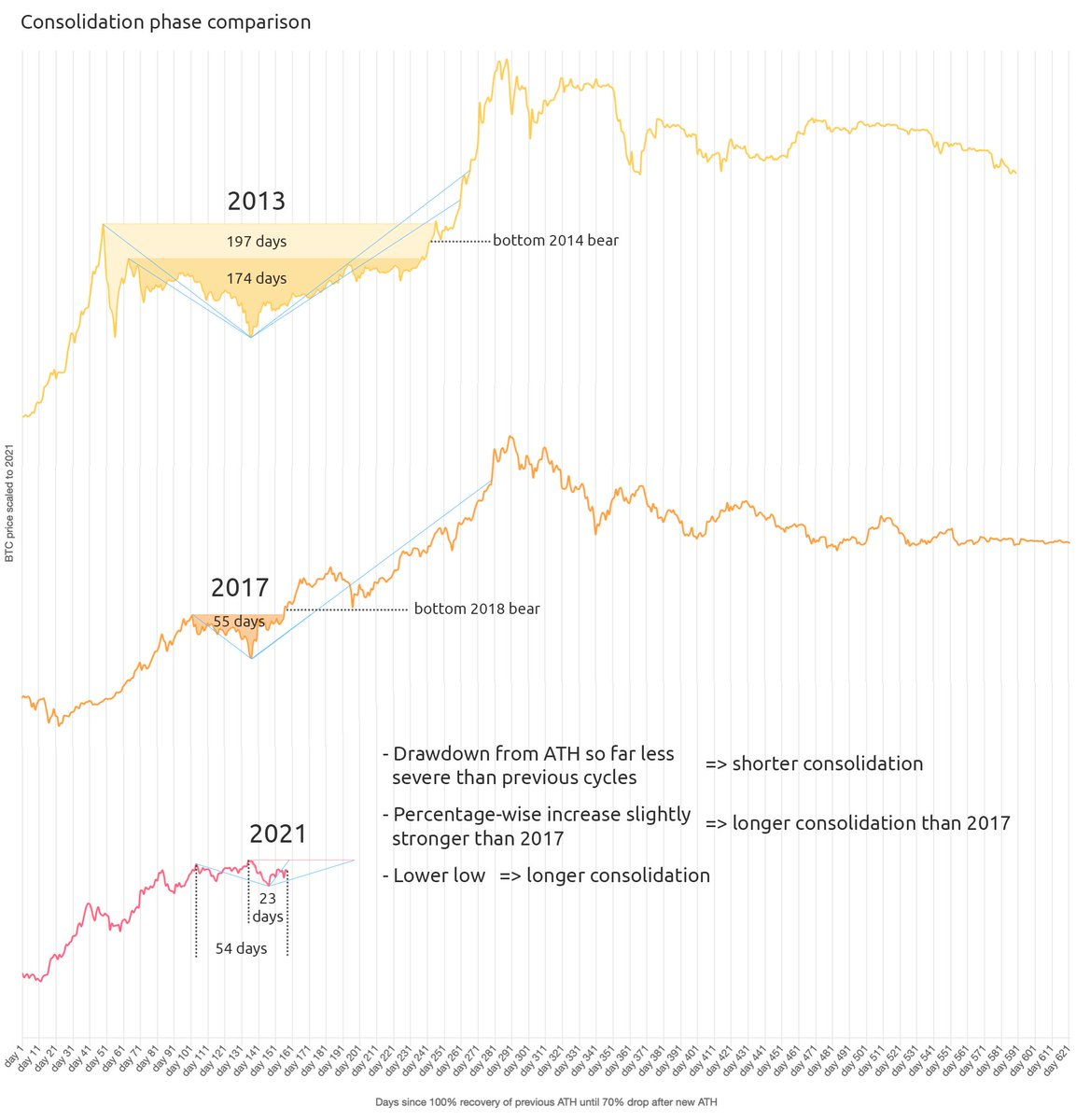

The weekly close was just above the pivotal level of $57,500. Bitcoin has remained within that range for 12 weeks now.

Comparing this price action with previous cycles, we see that this consolidation stage is a common pattern of bitcoin bull market cycles. In the 2017 cycle, the consolidation range lasted 55 days. In the 2013 cycle, it lasted 194 days. The consolidation around the $57,500 level has lasted 84 days so far this cycle.

Among the potential headwinds, bitcoin could have been impacted by Biden’s capital gains tax increase proposal. As tax laws are not typically retroactive, investors may have “jumped the gun” to realize the tax gain ahead of the change for next year. This could have impacted the best performing assets in their portfolios (like bitcoin). Cathie Wood also mentioned this had hurt “innovation” strategies in general. We’ll discuss the possibility of this new tax coming into effect in our What’s ahead for the week section.

As a potential tailwind, the dollar index has broken a critical level to the downside and it is displaying a familiar price-action pattern typically present in cyclical downturns for the index. With unemployment and inflation rates in the U.S. still far away from the Fed’s targets, it is looking increasingly likely that the dollar will continue to move lower. This is typically a positive catalyst for bitcoin.

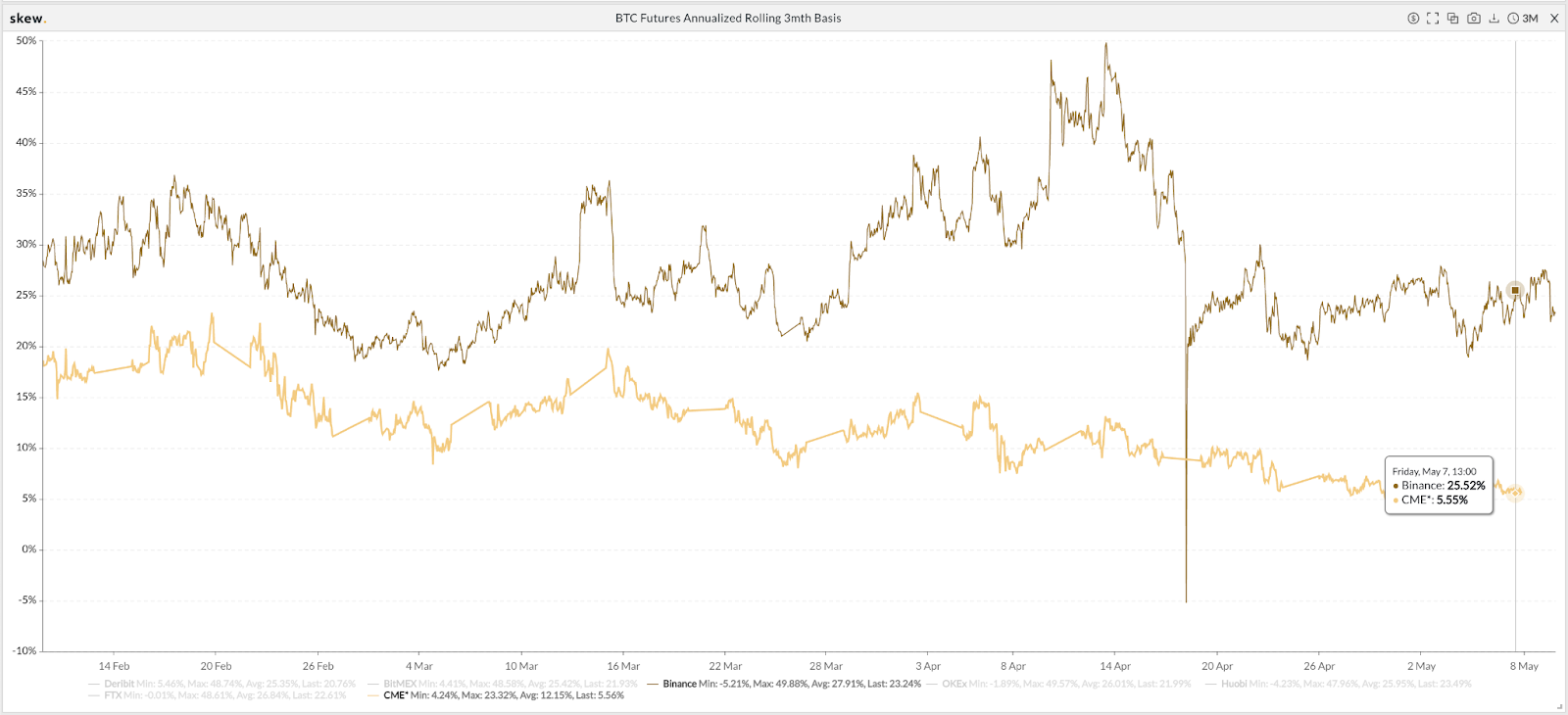

Signs of institutional activity continue to mount. The implied annualized futures premiums spread between the CME and Binance have widened from 10% to 20% over the last 3 months.

S&P 500: The S&P 500 closed the week at a fresh new all-time high of 4,234 points, +1.07% for the week. The sector rotation from technology into industrials is in full swing, as evidenced by the Dow Jones Industrial index breaking out to a new all-time high of 34,777, up +2.67%, and the Nasdaq closing the weekat 13,179 , down -1.02% .

Further evidence for the shift at play is what is happening with copper and lumber prices.

Copper prices are at 24-year highs and lumber prices have almost tripled since their pre-pandemic levels.

Quick update on the Russell 2000 index, it still has not broken out from that key 2,293 level, but it continues to stay within the “coiling” range that we defined last week. It looks ready to break out decisively into either direction.

Earnings season is starting to wind down but we still have Ali Baba, AirBnb and DoorDash reporting on Tuesday. There are also Federal Reserve Governor speeches on Tuesday at 9 AM and Thursday at 1 PM.

Gold: We’re seeing some signs of life in gold on the back of the breakdown in the dollar index.

Last week it had its biggest weekly gain of 2021, closing at $1,831/oz, up +3.53%.

The weekly close is very significant from a technical point of view. As seen above, the weekly close effectively “breaks away” from the down-trend channel that gold has been in since August 2020.

When these types of long-term directional channels break, they typically run on momentum. Gold is generally inversely correlated with the real rate of return of U.S. bonds.

This could mean that the market is pricing a lower real return on U.S. treasuries, which would be consistent with treasury interest rates being flat for almost 2 months now, and inflation indicators everywhere running higher. This trend may continue in the near term.

DeFi: It’s been all green in DeFi and Ethereum lately. Both saw fresh new all-time highs last week. The FTX DeFi index closed the week at 15,351 up 4.39%. Ethereum closed the week at $3,928, +33.07%.

Ethereum price is up 133% in the last 35 days.

Our view is that this could still have a tailwind effect of the EU bond offering on the Ethereum blockchain and the growth in DeFi. This trend seems to be picking up steam rather than slowing down.

Lastly, Dogecoin started selling off after Elon Musk’s SNL performance, being down 25% the following day but quickly recovering. The emergence of derivatives and a liquid “short” market will likely create knee-jerk price moves as the hype unwinds. Be careful out there!

Difficulty Commentary: The next difficulty adjustment is scheduled to kick in on Wednesday. It is currently projected to bring difficulty back up ~12% up to 23.13 TH.

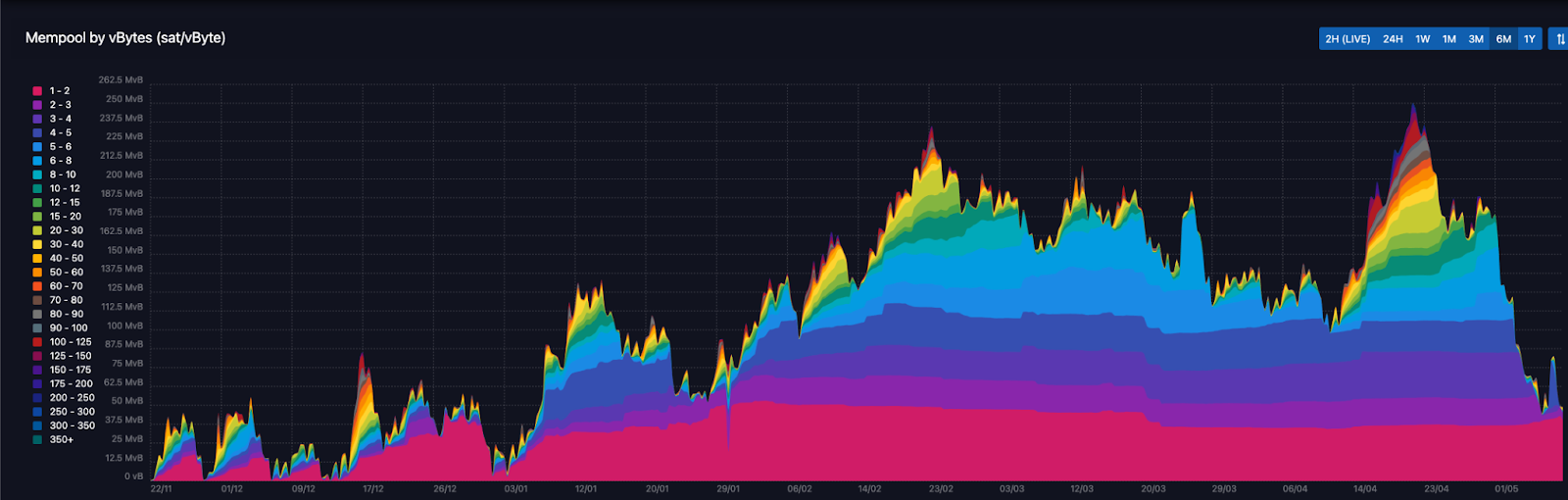

The mempool congestion has come down dramatically and so have transaction costs. Transaction fees have now come back down to about 70 sats/vbyte for next block confirmation, with 2-block estimates being 2 sats/vbyte! Just weeks ago we were at 250+ sats/vbyte for next block confirmation.

The way the Bitcoin network self-regulates through difficulty adjustments is awe-inspiring.

What's ahead for the week:

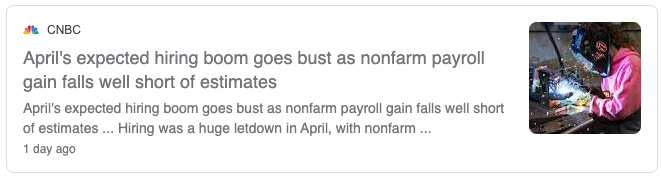

Last Friday we got a less-than-stellar employment update out of the U.S. with April’s numbers being way below analyst expectations.

Analysts were expecting an increase of over one million new jobs in the non-farm payroll numbers and the results came in at +266,000. Only ~25% of what was expected. April was also the month during which the last stimulus cheques were announced and deployed. At a high level, this could be interpreted as people who are being paid not to work, not working.

What else does this mean? It means that the Fed can’t lift the foot off the pedal just yet, and hence, we saw all markets rally on Friday after the jobs numbers came out.

Biden plans to pay for his new infrastructure stimulus package through a series of higher taxes. The biggest headwind for markets is the proposed increase in the capital gains tax rate from 22.8% to 41%. There are also proposed increases to the highest income bracket to 41%, and the corporate tax rate from 21% to 28%. Cathie Wood from Ark Invests believes the capital gains tax increase has a low probability of passing, given that the Democratic party has a razor thin majority in the house of representatives, and the midterm elections are on November 2nd, 2021. We agree.

The “d” word

We spend a lot of time discussing inflationary pressures. Today, we wanted to spend a second addressing “deflationary” pressures and how they play out in the markets.

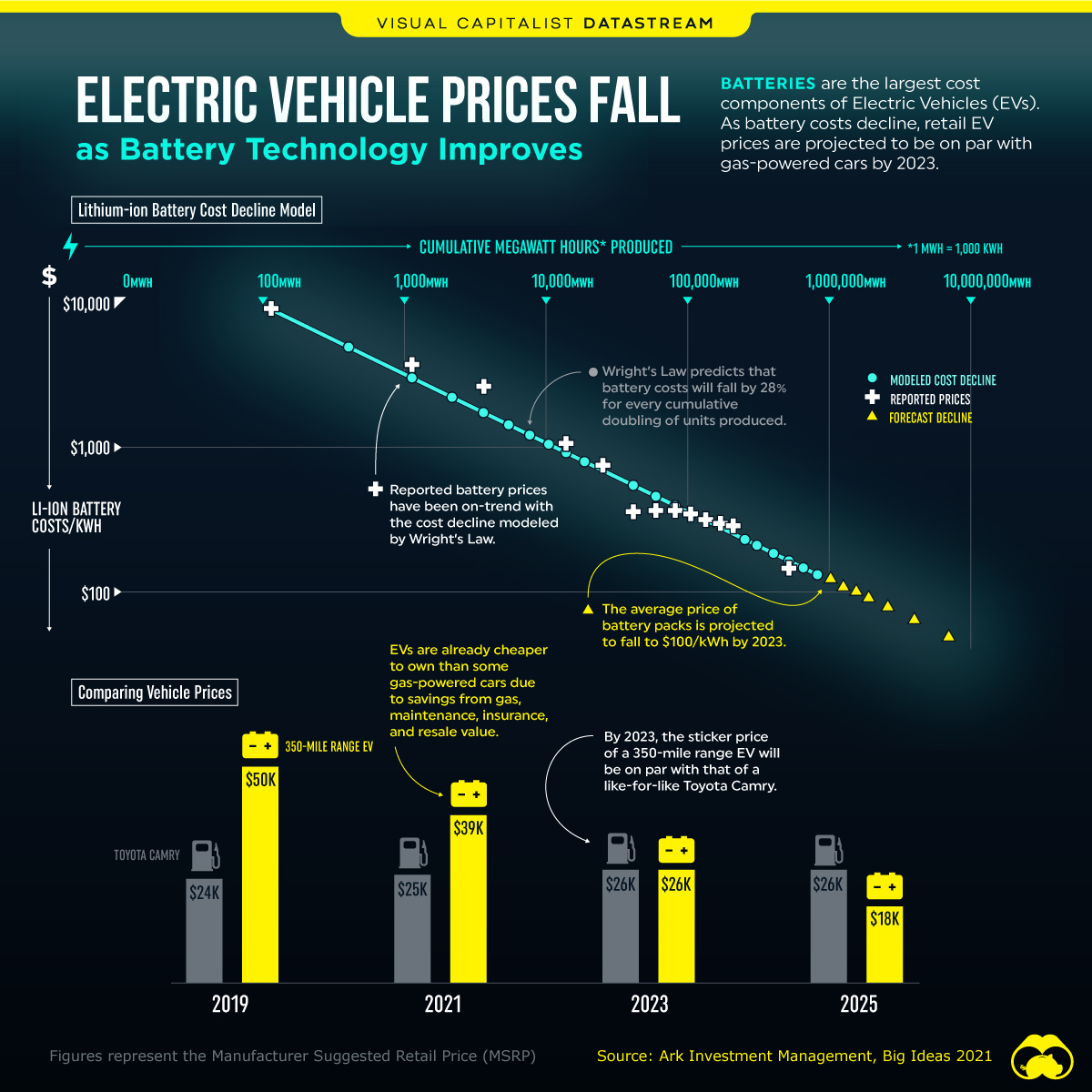

Innovation-driven deflation occurs when production costs decrease due to productivity gains. This is the type of deflation that has made TVs and computers cheaper and higher quality over time. It is also the same type of deflation pressure that is driving down the costs of battery packs and electric vehicles.

Disruption-based deflationary pressures are caused by the industries being disrupted lowering prices in their attempt to remain competitive. For example, car companies selling combustion-engine vehicles will be forced to lower the prices of their products to compete with cost-effective EVs. This puts overall downward pressure on prices.

These forces are always at play in the economy, and push back against inflationary-by-design fiat currency.

Cathie Wood at ArkInvest also sees a potential third source of deflation in commodities, excess inventory. This may kick in towards the end of the year, as she fears that manufacturers and suppliers are “double and triple ordering” now to meet strong demand forecasts - but will be stuck with too much inventory which will have deflationary pressures on prices.

Big week coming up, as always, we'll keep you posted on any relevant news throughout the week right here and from our Twitter account @hodlwithLedn

Canadian Central Banking Updates:

Current Target Interest Rate: 0.00 - 0.25%

Current Overnight Money Market Rate: 0.23%

Source: https://www.bankofcanada.ca/rates/

U.S. Central Banking Updates:

Current Fed Interest Target Rate: 0.00 - 0.25%

Current Effective Federal Funds Rate: 0.09%

Source: https://apps.newyorkfed.org/markets/autorates/fed%20funds

***

This article is intended for general information and discussion purposes only, it is not an offer or solicitation of any kind, and is not to be relied upon as constituting legal, financial, investment, tax or other professional advice. A professional advisor should be consulted regarding your specific situation. The information contained in this publication has been obtained from sources that we believe to be reliable, however we do not represent or warrant that such information is accurate or complete. Past performance and forecasts are not a reliable indicator of future performance.