Bitcoin

Bitcoin soared by more than 26% last week to a high of ~$28,500, slicing through key technical resistance levels on healthy volumes.

We have key economic data and a Fed decision on interest rates this week. This first section will focus on technical levels and market structure, and we will dive into the macroeconomic headlines and trends that drove the price action in the following sections.

As bitcoin price soared last week, bitcoin short positions continued to diminish. The price rally effectively liquidated many short positions, causing the price to “squeeze” higher. At the moment, bitcoin short positions on exchanges like Bitfinex remain near its historical lows.

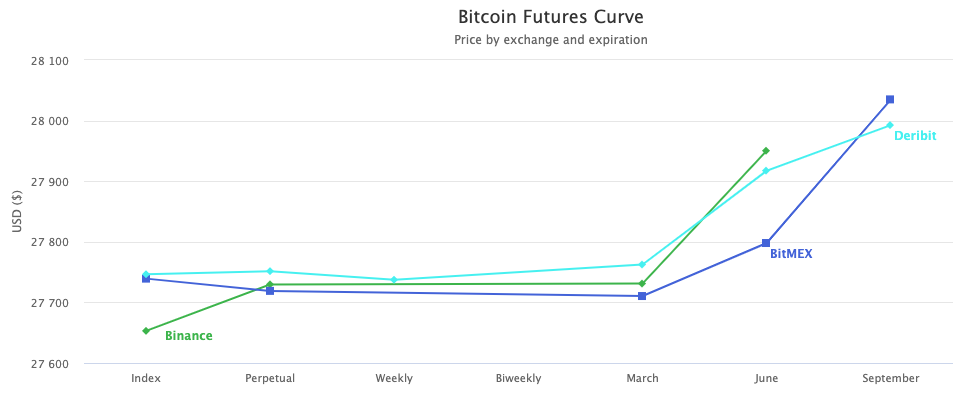

On the flip side, total open interest in bitcoin futures has soared by more than 15%, or $1.6 B - to a total of $11.8 B over the last week.

While it is unclear whether bitcoin futures positions are positioned net long or short, the positive funding rates on perpetual futures, and the healthy contango on the futures curve, suggest that a majority of these new positions are looking for upside, and are positioned net long.

Generally speaking, the buildup in bitcoin futures implies that investors have taken on leverage in their bitcoin positions, which could foreshadow price volatility in the near term.

Other sources for volatility in the week ahead will be the Fed decision on wednesday and Options Expiration day this Friday. Over 30,000 BTC worth of contracts will expire on Friday, and the “max pain” price - where most option contracts expire worthless, is approximately at $25,500.

Lastly, in terms of key technical levels, bitcoin sliced through the 200-week moving average price last week, which acted as an important resistance level, but should now “flip” to act as support. This level is currently around ~$25,300.

In terms of resistance, Bitcoin’s next key level to the upside will be $30,000, which has acted as support/resistance in the past. Beyond that, the next level up would be $35,000.

Digital Asset Markets:

1. Digital Gold

Back in our “Predictions for 2023” issue, we wrote that “Gold will top $2,000/oz as Central Banks and sovereign funds start allocating more of their reserves”. Serendipitously, gold crossed $2,000/oz on Monday as the World Economic Forum published an article detailing how Central Banks have used gold over the last 30 years… and the chart speaks for itself.

As you can see, until the Great Financial Crisis of 2007-2008, Central Banks were mostly selling gold (and buying other government’s debt). But the GFC triggered a rotation in asset holdings by some central banks - particularly in the emerging world.

Central banks have started rotating to hold increasingly less “inside money” - (instruments or assets controlled by a different government - like U.S. dollars and U.S. government bonds), and increasingly more “outside money”- (instruments or assets that are not under the control of one political group, like gold, oil, other commodities, and Bitcoin). This trend has been exacerbated by the U.S. sanctions of Russia and recent volatility around U.S. government bonds.

Bitcoin is easier to purchase, transport and much cheaper to store than physical gold. But perhaps most importantly, it is trading like gold.

Bitcoin’s 30-day price correlation to gold is now north of 70%. And it has been rallying as the shares of banks all over the world are collapsing (more on that next).

Every time bitcoin rallies alongside gold during times of uncertainty, the “digital gold” narrative strengthens. Take the headline below as an example:

So far, only publicly traded companies and El Salvador have added bitcoin to their balance sheets - but they will be joined by others… likely soon. And the trend to diversify from “inside money” to “outside money” is not just happening at a Central Bank level. Every time a person in Nigeria exchanges Nairas for Bitcoin, they are doing the same. Myself, and likely you - dear reader, already hold the best “outside money” there is - Bitcoin.

Macro:

2. Run on the [Central] Bank

I think the easiest way to explain what is happening right now is to paint a picture.

When the pandemic hit, everything got locked down, and people didn’t want to take risks. Even going to work was perceived as dangerous. So the Federal Reserve sent people money - literally, and made the “yield” of zero-risk assets (government bonds) equal 0%. They gave people money and said “go take risks”.

People happily complied. They bought stocks, real estate, cars, crypto, and many invested their dollars in yield products that were offering attractive returns. But they didn’t stop there - they also invested dollars in highly speculative schemes like Decentralized Finance “yield farming” - dogecoin, meme stocks of bankrupt companies and more. When the excesses were becoming too evident, and inflation was starting to appear, the Fed said that it would stop the party by raising the interest yield of the government debt. This made people’s debt more expensive, and increased the yield on the zero-risk assets.

The Fed did this so aggressively that variable mortgage rates more than doubled from 2.79% in 2021 to 6.34% in early 2023. This drained extra income from families all over the U.S.

Additionally, it made the return on government bonds explode higher. As an example, from November 2021 until March 2023, the yield on the 2-year bond more than 10Xed from ~0.5% to 5%. This made investing in “risk-free” U.S. treasury bonds very attractive. And so began the great “derisking” liquidity drain. Investors of all sizes that had access to U.S. treasury bonds began selling other assets and buying U.S. treasuries en-masse.

This triggered a series of runs… or, as we will explain now, one very big run.

The first “run” that we saw was on Decentralized Finance protocols, embodied by the collapse of the Terra/Luna protocol.

That first run exposed entities that were participating in this incredibly risky scheme, and that triggered a second run. Clients from Centralized Entities that were visibly involved with Terra/Luna started withdrawing their assets as a precaution. This led to the collapse of platforms like Celsius and continued until the FTX/Alameda collapse. Collectively, these events brought down many prominent players in the crypto industry.

The second run triggered a third run. Investors from banks that were exposed to crypto companies started selling their stock and withdrawing their deposits, which exposed a structural problem with the U.S. banking system: Banks had taken in deposits when interest rates were at 0%, and to earn income, they bought U.S. government bonds. As the Fed raised rates, the banks started accumulating large losses on those bonds. These losses would not materialize unless everyone wanted their money back… and people started asking for their money back. This led to the collapse of Silvergate bank, which was a prominent bank within the crypto industry.

The collapse of Silvergate Bank then led to clients and investors at other banks getting concerned, and within days, this triggered a fourth run - on smaller or regional U.S. banks. This led to the collapse of Silicon Valley bank, which had very little to do with crypto. Seeing this, the Fed had to step in to prevent contagion. To do so, it effectively insured the deposits of the affected banks, but it came short of guaranteeing the deposits from _all other_ banks. This led to people withdrawing funds from smaller regional banks to deposit the assets into larger “too-big-to-fail” banks, where they felt safer.

As a side note, Circle, the operator behind USDC, is now holding its cash reserves at the Bank of New York Mellon. This allows USDC holders to benefit from the safety of one of the oldest banks in the U.S. The rest of its USD reserves, around 77%, are directly invested in U.S. Treasury Bills.

Ok - back to the story. In response to the new incoming deposits from smaller banks, large U.S. banks got together and made a token deposit back into a smaller, troubled bank as a sign of support… yes, you are reading that right.

But the “deposit theater” by big banks, the Fed’s backstop of the affected banks, and standing a facility for other U.S. banks that may need help, was not enough to appease the masses.

As the week progressed, people kept withdrawing from small U.S. banks into larger U.S. banks, and the “run” quickly expanded overseas. Investors from all over the world started withdrawing funds from banks as well. Effectively, people wanted to withdraw their funds from any bank that did not have an implicit or explicit backstop from the Federal Reserve, and deposit them into a facility that did, like a very large bank deemed “too-big-to-fail”.

The poster child for the European Bank crisis became Credit Suisse. Its stock plummeted last week as depositors took their money out. This forced the Swiss National Bank to intervene over the weekend as it had to coordinate a “bailout” purchase of the troubled bank by one of its long-time competitors, UBS.

And it did not stop there. Investors worldwide have kept withdrawing funds from their local banks to convert them into U.S. dollars and deposit them in large U.S.-based institutions. This has caused the U.S. dollar to soar against other currencies. And the Fed had to step in once again to set up foreign exchange swap lines with select Central Banks over the weekend.

The goal of the swap lines is to remove pressure from FX rates by allowing central banks to swap currencies directly at predetermined rates. This allows one or both central banks to shore up the impact on the currency by absorbing some of the losses.

So - where do we go from here?

The swap lines may not be enough, and we may continue to see people worldwide withdraw deposits from their local banks to move them where they feel safer. Since most central banks followed the Fed’s footsteps, most banks face the same issue as U.S. banks - and they don’t have a Fed to backstop them.

It’s becoming increasingly evident to everyone that FIAT monetary policy is not about “expanding and contracting” the money supply - it’s about “selectively expanding it” only. The contraction periods are temporary and shallow - the expansion periods are long and steep. The trust in banks continues to erode along with trust in FIAT currencies. People want to save in a transparent instrument that cannot be manipulated - and thousands are finding that in bitcoin every day. Choose your savings instrument wisely. And if you’re saving in U.S. dollars, make sure you’re getting a great interest rate!

The Week Ahead 📰

The main event this week will be the Federal Reserve’s interest rate decision due on Wednesday at 2 PM EST. As per the CME’s FedWatch tool, investors see a 73% probability of a 0.25% interest rate hike - to a target rate of 5.00%. The probability for a 0.25% increase rose by 12% over the weekend after the emergency swap line announcement. The emergency swap lines could also be seen as the Fed opening avenues to balance USD demand flows as it prepares to move its rate higher than most other western Central Banks. For context, the European Central Bank increased rates by 0.50% last week to a target rate of 3.50%. This happens because investors are enticed to borrow Euros at 3.50% and convert them into USD to earn 5%. Thereby arbitraging the risk-free rates. This has an impact on currencies - which the Central Banks are trying to mitigate through the swap lines.

In addition to the Fed decision, we’ll get several speeches from the European Central Bank president Christine Lagarde, and a big options expiration Friday for Bitcoin with over 30,000 BTC worth of contracts expiring. The “maximum pain point” price where most contracts would expire worthless is near the $25,500 level. This level could act as a “magnet” should bitcoin be trading near it come Friday morning.

As always, here’s a summary of the events and data that could move markets in the week ahead:

Notice for Canadian Residents: As of January 4, 2023, Canadian clients will no longer be able to take out new B2X loans. As of February 1, 2023, Canadian clients will no longer be able to open a new BTC or USDC Savings Account, deposit BTC or USDC to existing Savings Accounts or earn yield on any existing BTC or USDC Savings Account balances.

Notice for U.S. Residents: Effective March 1, 2023, U.S. clients will not earn interest on any BTC and/or USDC balance in their Savings Accounts and/or Legacy Savings Accounts.

This article is intended for general information, educational and discussion purposes only, it is not an offer, inducement or solicitation of any kind, and is not to be relied upon as constituting legal, financial, investment, tax or other professional advice. This article is not directed to, and the information contained herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to law or regulation or prohibited by any reason whatsoever or that would subject Ledn and/or its affiliates to any registration or licensing requirement. This article is expressly not for distribution or dissemination in, and no Ledn product or service is being marketed or offered to residents of, the European Union, the United Kingdom, the United States of America or any jurisdiction in Canada, and such product or service may only be marketed or offered in such jurisdictions pursuant to applicable laws or reliance on regulatory exemptions. A professional advisor should be consulted regarding your specific situation. Digital assets are highly volatile and risky, are not legal tender, and are not backed by the government. The information contained in this publication has been obtained from sources that we believe to be reliable, however we do not represent or warrant that such information is accurate or complete. Past performance and forecasts are not a reliable indicator of future performance. Any opinions or estimates expressed herein are subject to change without notice. This article may contain views or opinions of the author that do not necessarily reflect the opinions, standards or policies of Ledn. We expressly disclaim all liability and all warranties of accuracy, completeness, merchantability or fitness for a particular purpose with respect to this article/communication. Read our Disclaimers at https://ledn.io/legal/disclaimers