.png?width=960&height=540&name=Banner%20%26%20LI%20-%20Sept%2011%20(1).png)

Ledn’s Weekly Hodl: The Loonie Under Fire

Week of Monday September 11th

Start earning up to 8.50% APY on your crypto with a Ledn Growth Account.

Bitcoin Market Analysis

Bitcoin price has remained nearly unchanged since August 21st, oscillating in the mid $25Ks over the last 3 weeks.

Another important consideration is that the U.S. dollar index has risen by +1.61% over the last 3 weeks, which is typically a headwind for all assets. Both Bitcoin and capital markets have shown resilience over the last 3 weeks considering that headwind.

The next big catalyst for markets will be the Fed’s next interest rate decision scheduled for September 20th. The CME’s FedWatch tool shows that investors see a 93% probability that the Fed announces no change to the interest rate - this would be the second pause in the cycle, since June’s interest rate decision.

While there hasn’t been much change in terms of Bitcoin’s price, lots has changed in the spot bitcoin ETF race. Last week a U.S. court ruled in favour of Grayscale, defeating the SEC and asking it to reconsider its rejection of Grayscale’s spot Bitcoin ETF application.

The news caused bitcoin to rally briefly to the $28K range, but it has given the gains back since.

However, the news does seem to have opened up the path for an imminent spot Bitcoin ETF approval - as the SEC is now running out of reasons to deny it. This development should allow for some price stability in Bitcoin, as investors may look to start accumulating opportunistically in anticipation of the ETF launches.

The optimism for a spot bitcoin ETF approval is also reflected in the wave of recent spot Ethereum ETF applications. Valkyrie, Vaneckm, and Ark Invest have submitted applications over the last few days.

The anticipation and excitement around the spot ETFs should be a tailwind for the industry in the near term.

Our Weekly Essay: The Loonie Under Fire

Loons are majestic aquatic birds native to Canada and North America. A Loon sits on Canada’s famous $1 coin, and it’s the reason people refer to the Canadian dollar as the “Loonie”. Loons, the birds, are protected from hunting– but the Loonie, as in the dollar, is fair game, and it’s coming under fire.

The Canadian dollar has lost almost -4% of its value relative to the USD over the last 57 days. In today’s essay we dive into what’s behind the move, and what could be next for the Loonie (and other world currencies).

Print away the pain

As many countries did during the COVID pandemic, Canada printed a lot of money to stimulate its economy. Since January 2020, the Canadian M2 money supply has increased by +33%. This means, 33% of all money in circulation in Canada was printed within the last 3 years.

As our dear readers now know very well, when a government prints inorganic money and injects it into the economy, and the supply of assets remains unchanged, the price of those assets, denominated in the money units will go up. Canada is a beautiful example of this:

Since Q1 2020, the prices of condo townhouses In Toronto have increased by… drumroll please: you guessed it! +33%

As a further example, single detached homes in Toronto increased by +45% over the same period.

But it’s not just Toronto - Vancouver detached home prices also rose by +30%. Funny coincidence, right?

It’s almost as if it’s not the value of the homes that is rising, but the value of the Canadian dollar that’s eroding away…

We know that admitting that the government debases the currency arbitrarily does not sit well with the voting population. So, it can never be “the Government’s” fault. Every time prices soar higher, a convenient scapegoat is selected. In the case of Canadian real estate, it’s foreign buyers who get to play the bad guy this time:

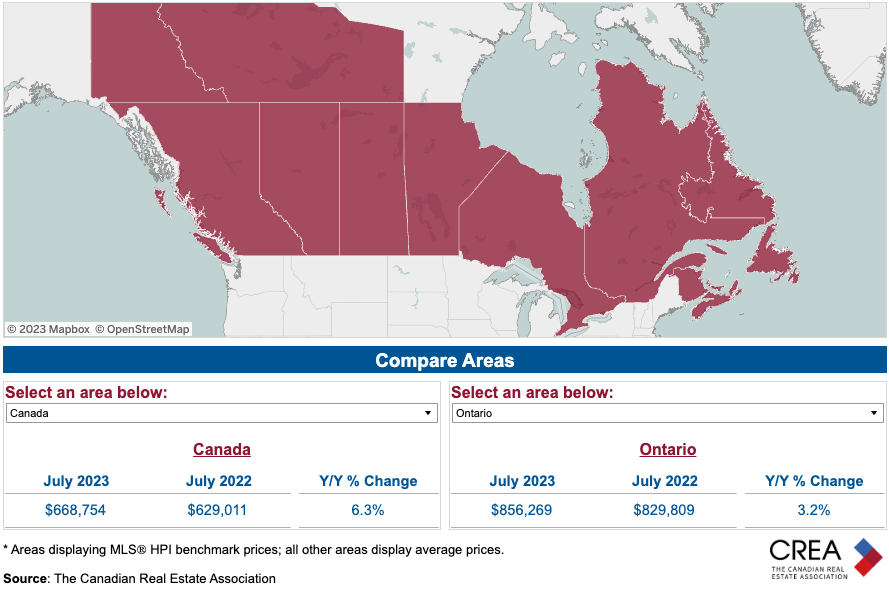

Even so, despite the Bank of Canada’s best efforts to squeeze Canadians out of their mortgages, real estate prices in Canada are still higher than they were a year ago:

However, these gains can be deceiving. Since July 2022 until today, the Canadian dollar has lost almost 5% of its value vs. the USD. Meaning that in real terms, the value of Canadian real estate on average is flat, at best.

The Golden [Canadian] Geese

There are 2 big drivers of strength to the Canadian economy, and the Loonie: strong immigration, and oil prices.

Let’s cover immigration first - more qualified migration means more human resources, more spending, and more taxes. Especially if they come with a desired set of skills, and financial resources to get settled. Much of Canada’s migration is like this, as the only land border it has is with the U.S. And it’s very far from countries suffering from a migration crisis.

Back in 2022, in the midst of a labour shortage, everyone was clamouring more immigrants. The above article references one of Canada’s top banks describing immigration as ‘a form of economic stimulus’. Canada wanted immigrants, and they got just that!

This wave of new Canadians supported the local economy and the Loonie for much of 2022 and early 2023. More on this later.

Now to oil: to understand why oil prices are so important for the Loonie we have to look at Canada’s exports. 36% of all of Canada’s exports are made up of “Energy, Crude, and Crude Bitumen”. All closely related to the price of oil. Therefore, it’s no surprise that the Loonie has a positive correlation with the price of oil.

Oil prices have been quite stable throughout 2023, and in fact are slightly higher year-to-date. This has translated into stability for the Loonie as well.

However, both of these trends are now facing headwinds…more on this next.

Killing the Golden [Canadian] Geese

As we mentioned above, the debasement of the Canadian dollar has made house prices soar. To make matters worse, the Canadian Central Bank has jacked up interest rates from 0% to 5% in just over a year, making rents soar as well.

Economic theory suggests that if you increase the price of a good or service, demand for it should drop. However, when that good or service is housing, and you are increasing the population by >3%+ per year, demand for a place to live will be very resilient. This is reflected in the market through strong real estate prices as we covered above, and in the rental market you have record-high costs…

paired with record-low vacancy rates:

So, naturally, this has driven a narrative shift around immigration:

In plain English, a housing affordability crisis engineered by interest rate manipulation has put a target on the back of immigrants, and now Canadian public opinion is starting to turn on the idea of immigration. This is resulting in political pressure to “do something about it”. If Canada shuts its doors to immigration, it will axe one of the main drivers of strength for the Loonie.

With regards to oil, the big threat to lower oil prices is a global recession. Demand out of China has cooled recently due to economic weakness (which the government is trying to address through stimulus).

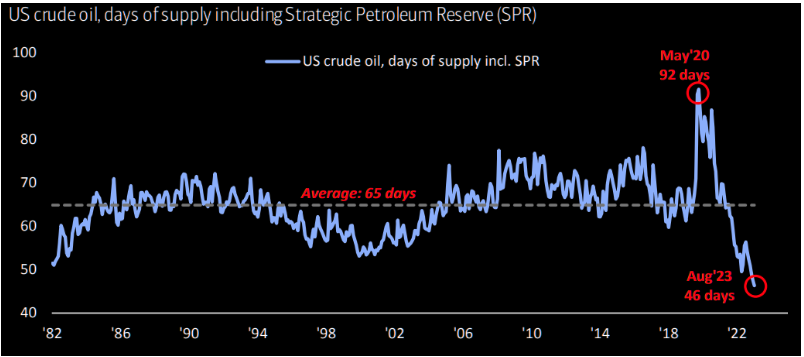

However, oil prices have a natural “put” option in the near term, thanks to the status of the U.S. Strategic Petroleum reserves. Chart credit to @KobeissiLetter

In simple English, the U.S. needs to repurchase a lot of oil to refill its reserves, and this demand adds price stability for oil in the near term.

Political pressure on the Canadian Central Bank

While high interest rates have slowed down inflation, they have done so at the expense of a housing affordability and cost of living crisis.

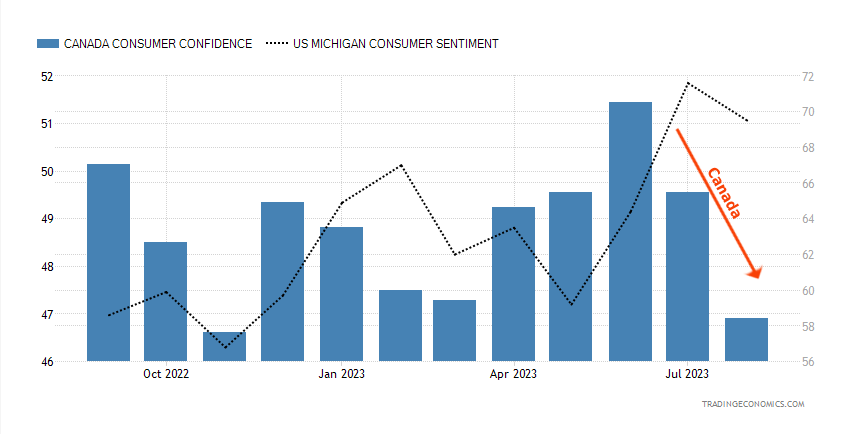

The Canadian Consumer Confidence index has diverged materially from the it’s U.S. equivalent over the last 3 months - suggesting that Canadians are feeling the pain of high interest rates much more than Americans.

The message has now reached politicians, who are openly calling on the Bank of Canada to stop interest rate hikes.

Over the last few weeks, three Provincial Premiers have urged the Bank of Canada to stop interest rate hikes:

The Bank of Canada seems to have listened, by electing to keep rates steady last week, although it has left the door open for potential further hikes.

Damned if you do, Damned if you don't

The Canadian Central bank is in a tight spot.

If they don't raise rates, the Loonie will tumble, and inflation will return. This would also have the optical illusion of “stabilizing” the housing market in Canadian dollar terms. (even though the owners will be losing real value in USD terms). The result of this option is “medium” political pressure.

If they do raise rates, they will make housing and rentals even less affordable - with builders building even less housing for future growth. In a market where consumers are already feeling squeezed, and there are few places to go (there’s no vacancy!) - this could drive many to the edge. The result of this option would be “high” political pressure.

Because politicians typically choose the path of least resistance, it’s probable that the Canadian dollar will come under pressure for the rest of the year - absent a massive rally in oil prices.

Canada is just one of many examples of economies and Central Banks facing pressure to keep up with the Federal Reserve’s pace. Many currencies will come under pressure versus the dollar as the global interest rate cycle turns the corner. Inflation has been “sleeping” in the great white north as of late, but that could all change very quickly.

HODL.

Notice for Canadian Residents: As of August 3, 2023, any Canadian BTC or USDC Savings Account is transitioned into a new non-interest earning BTC or USDC Transaction Account for the purposes of allowing Canadian clients to manage their Ledn loans.

Notice for U.S. Residents: As of August 3, 2023, any U.S. BTC or USDC Savings Account is transitioned into a new non-interest earning BTC or USDC Transaction Account. On that date, the account balance in any U.S. Legacy Savings Accounts will remain in such accounts and continue to be non-interest earning.

This article is intended for general information, educational and discussion purposes only, it is not an offer, inducement or solicitation of any kind, and is not to be relied upon as constituting legal, financial, investment, tax or other professional advice. This article is not directed to, and the information contained herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to law or regulation or prohibited by any reason whatsoever or that would subject Ledn and/or its affiliates to any registration or licensing requirement. This article is expressly not for distribution or dissemination in, and no Ledn product or service is being marketed or offered to residents of, the European Union, the United Kingdom, the United States of America or any jurisdiction in Canada, and such product or service may only be marketed or offered in such jurisdictions pursuant to applicable laws or reliance on regulatory exemptions. A professional advisor should be consulted regarding your specific situation. Digital assets are highly volatile and risky, are not legal tender, and are not backed by the government. The information contained in this publication has been obtained from sources that we believe to be reliable, however we do not represent or warrant that such information is accurate or complete. Past performance and forecasts are not a reliable indicator of future performance. Any opinions or estimates expressed herein are subject to change without notice. This article may contain views or opinions of the author that do not necessarily reflect the opinions, standards or policies of Ledn. We expressly disclaim all liability and all warranties of accuracy, completeness, merchantability or fitness for a particular purpose with respect to this article/communication. Read our Disclaimers at https://ledn.io/legal/disclaimers