Market Commentary

Bitcoin price has been relatively muted over the last 2 weeks, but that could drastically change as we head into the last weeks of the year. In today’s dispatch, we highlight 3 key drivers that could impact bitcoin during what’s left of the year.

- Newsflow from FTX aftermath:

It’s now been almost 3 weeks since FTX stopped processing withdrawals on November 11th, but the negative headlines haven’t stopped.

On the same day that FTX announced it was no longer

ls, BlockFi, a crypto lending platform with close ties to FTX, also announced it would stop processing withdrawals.

Just five days later, on November 16th, Genesis Capital, a large institutional lender, also announced that it would be halting withdrawals.

Not surprisingly, this led to a wave of “contagion” headlines and fears among consumers - some still traumatized by the previous 3AC collapse which led to other platforms pausing withdrawals and ultimately entering into bankruptcy.

While the dust seems to have settled a bit over the last 2 weeks, yesterday the news broke that Blockfi had gone into bankruptcy. While many expected the news, it still added selling pressure to the markets as the headlines made their way through mainstream media.

The biggest remaining question mark in terms of potential newsflow is the current case with Genesis Capital. With withdrawals halted, its parent company is looking for financing to resume operations.

While many industry observers speculate that Mr. Barry Silbert should have no problem finding the necessary funding, recent weeks have shown us that anything can happen.

As if the current environment was not complex enough, Barron’s reported last week that Genesis Capital was being probed by U.S. regulators.

- Macroeconomic Headwinds

As the U.S. jobs market and housing markets are starting to show signs of economic deterioration, the Federal Reserve is preparing to once again hike interest rates at its upcoming December 15th meeting.

This is akin to the Fed leaving rates at 0% and continuing to buy mortgage-backed securities and treasuries just over a year ago, when the real estate market was rallying by 18% year-over-year and unemployment was at record lows - but in reverse.

To borrow an analogy from Pentoshi on Twitter, rising interest rates is like driving over a nail - your tire may continue to run fine for a while, and you - the driver, may not even notice right away. But eventually, your steering wheel will get wobbly and your car will stop.

This means that we should expect to see continued deterioration of the U.S. and global economy in the coming weeks and months as a result of the coordinated efforts by western central banks to tame inflation.

- On-chain Indicators

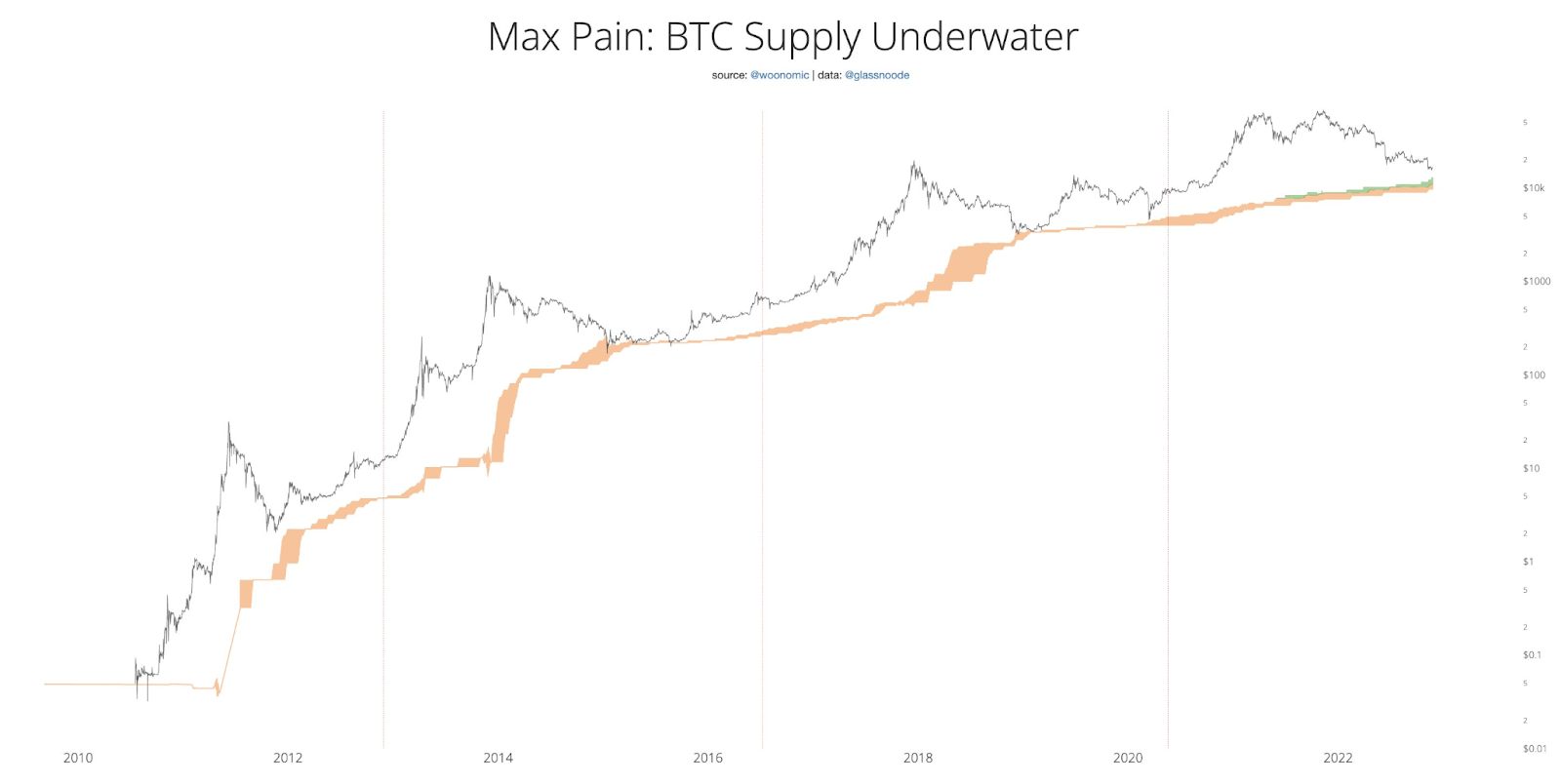

While the newsflow and macro outlook are playing against bitcoin price in the near term, the bright side is that on-chain analytics suggest that the bottom in terms of price could be near.

The “Max Pain” model highlights that bitcoin cycle bottoms tend to be reached with approximately 58-61% of the circulating supply being “under water”. We are rapidly approaching that level, with the range being between $12k-$14k.

Similar on-chain models are consistent with the $12-$14k range as a suggested bottom given previous cycles.

This also marries well with the narrative that U.S. equity markets have further room to fall, given their current levels and the year-end targets from top bank analysts. The S&P is still north of 3,900 points, with experts calling for levels near 3,600 to close out the year.

In summary, the current setup suggests that it could be a rocky month to end the year. However, investor sentiment could turn early next year as the Fed tapers interest rates and stops tightening conditions further.

S&P 500

Equity markets continue to defy gravity and hold on to their gains after October’s soft inflation report. It’s almost as if they forgot that the Fed has taken rates from 0% to 4%, draining cash from the economy and obliterating anyone’s chances of getting a mortgage.

Last week’s FOMC meeting minutes showed 2 interesting trends: 1) Fed officials are on board to raise rates higher in December, and 2) Fed officials support a higher terminal interest rate than previously discussed.

The estimates discussed for “peak interest rates” ranged from 4.25% to 6% - that’s a wide band, but 16 out of 28 respondents to an additional question on rates said that the risk was that rates would peak higher and faster than their current estimates.

In terms of year-end targets for the S&P 500, Bank of America, JP Morgan and Morgan Stanley converge around the 3,600 mark. However, Goldman Sachs’ year-end target is 4,000. In any scenario, no estimate suggests that the S&P will be higher than where it is currently trading.

Another recent curveball that has been thrown at global equities is the current social unrest in China.

This is a rare occurrence. For context, it is very rare to hear negative news outside of China. Their government heavily controls and restricts their local media, and strongly influences any headlines that make it to international media.

The country has gone so far as to censor any footage from the world cup that shows unmasked people in stadiums.

China has long touted an “iron grip” on its society. But as the most populous country in the world, widespread unrest would be very hard to control.

The current lockdowns and social unrest have many economists calling for future supply chain disruptions that would further fuel inflation. This will be one more variable for investors to navigate in an already complex market.

Let’s not forget that we still have an active war in Ukraine and Europe is in a very vulnerable position as the dead of winter sets in. It could be a rocky end to the year in equities.

Gold

Gold prices have managed to hold on to their gains and it continues to trade above $1,700/oz. Year-to-date, gold is down about 5% in U.S. dollar terms, but keep in mind that the U.S. dollar index is up above 9% year-to-date.

I’d chalk that up as a win for gold, working as intended in a rising rates environment that has crushed equities and bonds alike.

The buzz around gold has been growing recently, with none other than Mr. Nouriel Roubini, aka Doctor Doom, named it as one of the few assets that could perform well in the upcoming antagonistic economic environment that he predicts is coming.

Mr. Roubini argues that gold has been held back by rising interest rates from western Central Banks. He argues that once Central Banks “wimp out” and bend a knee on interest rates, gold should be poised to do quite well.

Last week we noted how a select group of Central Banks was adding more gold to their reserves, and this week we saw a very interesting headline out of Ghana.

They are developing a plan with the UAE to allegedly trade gold for oil, without the need of going through the U.S. dollar. This arrangement may foreshadow more to come from commodity-producing countries that trade each others’ needs.

DeFi

As the year enters its last trading month, Ethereum and Bitcoin are neck and neck in terms of annual results to-date. Ethereum priced in BTC terms is up just +3.62% for the year.

While still stuck in the historical resistance of 0.08 BTC, eth/btc continues to trade at the high end of the range, and it’s doing so in a downmarket. Typically, the upper levels got tested in bull markets - now they are being tested in the dead of a bear market.

It is important to consider what happens in bear markets because it can give you clues as to how assets could behave once sentiment improves again. Ethereum benefits from several trends over bitcoin once retail investors come back in full force. Beyond the allure of staking yield and the token and project ecosystem it facilitates, one important benefit over bitcoin is, believe it or not, its unit price.

Retail investors prefer to buy assets that have small price tags, as they can buy more “units” and a small change in price can represent a large change in percentage terms. Of course, any seasoned investor will tell you that it is impossible to tell whether an asset is cheap or expensive based on the stock price, if you’re not told how many shares are outstanding. There’s a reason companies do stock-splits.

Mining

Bitcoin miners continue to feel the pain, with the focus being on the publicly traded miners.

Last week, Bloomberg reported that Core Scientific had lost over $1.7 Billion this year alone, and them - along with every other bitcoin mining company, are seeing record low revenues, combined with record high mining difficulty and energy costs.

As we reported last week, distress also creates opportunities, and this could be the time for some consolidation in the industry. Bloomberg wrote an interesting article about Mergers and Acquisitions in the mining industry during difficult market conditions.

Despite all of the doom and gloom, there is positive news on the horizon for bitcoin miners. Mining difficulty is projected to drop by about 6% a week from now, which should help their revenues.

What's ahead for the week

This week we will get 5 Fed speeches, including one from Jerome Powell, Chairman of the Fed. This is happening ahead of the upcoming FOMC meeting on December 14th, where they are likely going to increase interest rates by another 50 basis points. They will likely be setting the narrative for their upcoming decision.

The most wanted man in crypto is also scheduled to make a public appearance this week. Mr. Sam Bankman-Fried is scheduled to participate in an upcoming New York Times “Dealbook” event this Wednesday. The timing is yet to be determined, but you can certainly expect lightspeed coverage of whatever is said.

The wildcard news item for the weeks ahead will be the outcome of Genesis Capital and Digital Currency Group. While the headlines have been drowned in recent days, they will no doubt make headlines again when a decision is announced - regardless of the outcome. A positive outcome should bode well for bitcoin prices, and vice versa.

Here’s a summary of the events and data that could move markets in the week ahead:

Tuesday

09:00 AM EST - S&P Case Shiller U.S. Home Price Index - previous was -9.8% year-over-year.

Wednesday

08:50 AM EST - Fed Speech - Michelle Bowman, Fed Governor

12:35 PM EST - Fed Speech - Melissa Cook, Fed Governor

01.30 PM EST - Fed Speech - Jerome Powell, Chairman of the Fed at the Brookings Institution

TBD - Sam Bankman-Fried to speak at the New York Times Dealbook event.

Thursday

08:30 AM EST - U.S. Initial and Continuing Jobless Claims (Unemployment reading)

03:00 PM EST - Fed Speech - Michelle Barr

Friday

10:15 AM EST - Fed Speech - Charles Evans, Fed Governor

It's a big week coming up, and as always, we'll keep you posted on any relevant news throughout the week right here and from our Twitter account.

_____________

Notice for U.S. Residents: Effective April 4, 2022, U.S. clients will no longer be able to earn interest on any newly deposited funds in their BTC and/or USDC Savings Accounts, where available; however, they will continue to earn interest on their pre-existing balances in their BTC and/or USDC Legacy Savings Accounts.

This article is intended for general information, educational and discussion purposes only, it is not an offer, inducement or solicitation of any kind, and is not to be relied upon as constituting legal, financial, investment, tax or other professional advice. This article is not directed to, and the information contained herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to law or regulation or prohibited by any reason whatsoever or that would subject Ledn and/or its affiliates to any registration or licensing requirement. This article is expressly not for distribution or dissemination in, and no Ledn product or service is being marketed or offered to residents of, the European Union, the United Kingdom, the United States of America or any jurisdiction in Canada, and such product or service may only be marketed or offered in such jurisdictions pursuant to applicable laws or reliance on regulatory exemptions. A professional advisor should be consulted regarding your specific situation. Digital assets are highly volatile and risky, are not legal tender, and are not backed by the government. The information contained in this publication has been obtained from sources that we believe to be reliable, however we do not represent or warrant that such information is accurate or complete. Past performance and forecasts are not a reliable indicator of future performance. Any opinions or estimates expressed herein are subject to change without notice. This article may contain views or opinions of the author that do not necessarily reflect the opinions, standards or policies of Ledn. We expressly disclaim all liability and all warranties of accuracy, completeness, merchantability or fitness for a particular purpose with respect to this article/communication. Read our Disclaimers at https://ledn.io/legal/disclaimers