.png?width=1600&height=900&name=How%20to%20Borrow%20Against%20Crypto%20(1).png)

Borrowing against cryptocurrency can seem complicated at first, especially if your experience with crypto so far has been buying and holding. However, it’s actually fairly straightforward. This guide will simplify the process and explain how crypto-backed loans work, helping you decide if they are the right choice for you.

TL;DR: What You’ll Learn in This Guide

This guide provides a clear overview of how to borrow against cryptocurrency, including:

- The basics of crypto-backed loans and how they differ from loans to purchase crypto.

- A step-by-step explanation of the borrowing process, from choosing a platform to receiving funds.

- The different types of crypto loans, including centralised, decentralised, margin lending, and stablecoin loans.

- Key advantages, such as retaining your crypto, avoiding credit checks, and potential tax benefits.

- Risks, including market volatility, margin calls, and platform security concerns.

- Alternatives to borrowing, such as selling crypto, staking, or using traditional loans.

What is a Crypto Loan?

A crypto loan involves borrowing funds by using cryptocurrency as collateral. These loans typically fall into two categories:

1. Crypto-Backed Loans

You pledge your cryptocurrency as collateral to secure a loan, usually disbursed in fiat currency or stablecoins.

2. Loans to Purchase Crypto

You borrow fiat money specifically to buy cryptocurrency.

This guide focuses on crypto-backed loans, how they function and the key steps to get started.

Read more: What are Bitcoin Loans? And How Do They Work?

What is a Crypto-Backed Loan?

A crypto-backed loan allows you to borrow money or stablecoins by using your cryptocurrency as collateral. This means your crypto assets, such as Bitcoin, Ethereum, or other tokens, secure the loan. Some platforms even accept NFTs as collateral, though this is uncommon.

The loaned funds can be issued in cryptocurrency or fiat currency, depending on the platform and your preferences.

How do Crypto Loans Work?

Crypto-backed loans use your cryptocurrency as collateral to borrow funds, which can be in fiat or crypto (such as stablecoins). After providing your collateral, you'll receive the loan along with repayment terms, including deadlines and consequences for missed payments.

While the general process is consistent across platforms, the specifics can vary.

Key factors to consider include:

Repayment Terms

The time allowed to repay and the applicable interest rates.

Service Type

Centralized and decentralized lending providers operate differently:

Centralized Providers

Support fiat and crypto loans, often provide customer service, and may have slightly longer approval times. The fastest platforms issue loans within an hour, but some take several days or weeks.

Decentralized Providers

Operate entirely in crypto with no human intervention, meaning instant approval and zero wait times. However, there’s typically no customer support.

How Do You Borrow Against Crypto?

Borrowing crypto involves using your cryptocurrency as collateral to secure a loan. Most lending platforms allow this, even if you're borrowing in cryptocurrency. Here's a simplified guide to help you through the process.

Read more: Understanding Crypto Loans: The Ultimate Guide

How to Borrow Crypto in 5 Steps?

Borrowing crypto involves using your cryptocurrency as collateral to secure a loan. Most lending platforms allow this, even if you're borrowing in cryptocurrency. Here's a simplified guide to help you through the process.

.png?width=1600&height=900&name=How%20to%20Borrow%20Against%20Crypto%20(2).png)

1. Select a Borrowing Platform

The first step is selecting a lending provider that meets your needs. This can require research to compare fees, loan-to-value (LTV) ratios, interest rates, and security. Picking the right platform simplifies the rest of the process.

Read more: 15 Best Crypto Loan Platforms

2. Choose your Collateral

Select the cryptocurrency you’ll use as collateral. Popular options include Bitcoin, Ethereum, USDC, and USDT, but supported assets vary by provider. Some platforms let you combine multiple currencies as collateral.

3. Decide How Much to Borrow

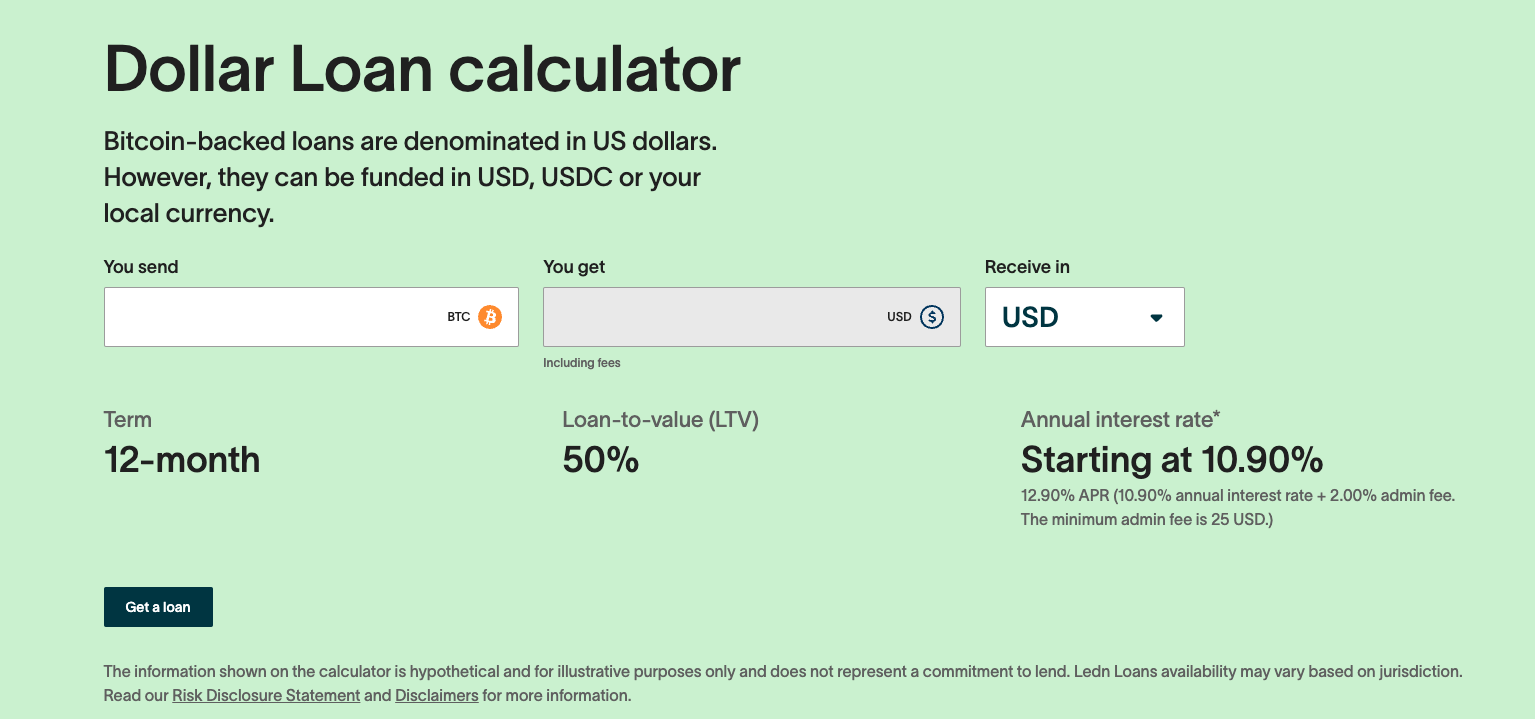

Determine the loan amount based on the LTV ratio offered by the provider. Most crypto loans are over-collateralized, meaning the loan amount will be less than the collateral you provide.

For example, if you use 1 BTC as collateral and the LTV is 50%, you can borrow the equivalent of 0.5 BTC in fiat or stablecoins.

Higher LTV ratios allow you to borrow more but typically come with higher interest rates.

Look for a balance between a fair LTV ratio and transparency from the provider. Beware of overly generous offers, as they may indicate risks with the lender’s practices.

See what you could borrow with this Loan Calculator.

4. Connect Your Crypto Wallet

Link your crypto wallet to the platform to facilitate the loan process.

- Decentralised Platforms: Use your wallet to sign into the network and interact with smart contracts.

- Centralised Platforms: Share your wallet’s public key to verify your holdings.

5. Provide Collateral and Receive Funds

Once you’ve reviewed the terms and are satisfied with the LTV and interest rates, transfer your collateral.

Related Content: CeFi vs DeFi - Key Differences Explained

Different Types of Crypto Loans

Crypto loans come in a few forms, each designed to meet different needs and preferences. Here's an overview of the most common options.

Centralized Crypto Loans

Centralised crypto loans are managed by organisations rather than automated systems. These loans can be disbursed in fiat or cryptocurrency and often support a wide range of assets, making them ideal for users seeking customer support, fiat integration, or flexible terms.

Decentralized Crypto Loans

Decentralized crypto loans, on the other hand, rely on blockchain-based smart contracts. These platforms operate exclusively within the crypto ecosystem, typically supporting tokens compatible with their blockchain (e.g., Ethereum-based tokens). These loans are fully automated, anonymous, and often processed instantly, appealing to crypto-native users.

Margin Lending

Margin lending is a specialised option for traders who want to borrow funds for investment purposes. Often integrated into exchanges, these loans allow users to leverage their holdings for trading activities, making them most suitable for experienced investors.

Stablecoin Lending

Stablecoin lending offers stability, either by using stablecoins as collateral or receiving stablecoins as loaned funds. Since stablecoins are pegged to fiat currencies, they reduce exposure to crypto volatility and are ideal for those seeking predictable financial transactions.

Peer-to-Peer Crypto Loans

Peer-to-peer (P2P) loans involve direct agreements between individuals, facilitated by smart contracts. These decentralised setups eliminate intermediaries, with funds securely locked and released as per the agreed terms, making this option attractive for those who prefer decentralised transactions.

Related content: How Crypto P2P Lending Works

Crypto-Backed Fiat Loans

Finally, crypto-backed fiat loans provide a way to access traditional currency without selling your crypto assets. Only available through centralised platforms, these loans are ideal for individuals who need cash for essentials while holding onto their crypto for potential future gains.

Pros and Cons of Crypto Loans

Let's look at the pros and cons of using crypto loans. This will also help you understand why people borrow crypto, and what to watch out for.

Pros of Crypto Loans

Retain Ownership

Crypto loans allow you to keep your digital assets while using them as collateral, so you don’t need to sell and risk missing out on potential future gains.

Potential Tax Benefits

Depending on your jurisdiction, holding onto your crypto instead of selling it can help you avoid capital gains taxes.

Easier Access Compared to Traditional Loans

Crypto loans are generally more accessible, catering to people who are unbanked or underbanked, with fewer eligibility requirements and faster approvals.

No Impact on Credit Score

Most crypto loan providers do not perform credit checks or use traditional credit rating systems, ensuring your credit score remains unaffected.

Simpler Approval Process

Loan terms are typically determined by the loan-to-value (LTV) ratio and the value of your collateral, not your financial history or creditworthiness.

Cons of Crypto Loans

Risk of Insolvency

A number of high-profile crypto lending platforms have collapsed, putting customer collateral at risk. Choosing a reliable provider with a strong track record and transparent practices will mitigate this risk.

Potential Collateral Value Increases

If your crypto rises in value while held as collateral, some lenders might charge additional fees or impose stricter terms to release it. Reputable platforms don’t do this, but it's best to check before committing.

Market Volatility Risks

If the value of your collateral drops significantly, you may face a margin call, requiring you to add more collateral or risk liquidation of your assets.

Lack of Consumer Protections

Unlike traditional financial systems, crypto lending lacks robust regulations and consumer protections, increasing the risk of scams or fraud.

Dependence on Platform Security

The safety of your collateral depends on the lender’s security measures. Hacks or security breaches can result in loss of funds, particularly with decentralised platforms.

Alternatives to Borrowing Against Your Crypto

Crypto lending isn’t suitable for everyone, so it’s worth exploring other options.

Here are a few alternatives:

Selling Your Crypto

Liquidating your crypto assets and converting them to fiat is a straightforward option, especially if you’re not worried about missing out on potential future gains. Selling eliminates the stress of repayment and allows you to receive nearly the full value of your crypto (minus transaction fees).

Staking

For holders of compatible cryptocurrencies, staking is a way to earn passive income by locking coins on the blockchain. Staked assets help validate transactions and secure the network, earning you rewards over time. However, staking isn’t available for all cryptocurrencies (e.g., Bitcoin doesn’t support it), and returns can take months or years to materialise, making it unsuitable for immediate financial needs.

Traditional Loans

The most common setup for traditional loans is secured loans, where borrowers use collateral such as real estate, vehicles, or savings accounts to guarantee repayment. Loan amounts are determined by the loan-to-value (LTV) ratio, typically 50%-90% of the collateral's value. Secured loans offer lower interest rates, influenced by credit scores, loan terms, and market conditions. Repayment is usually structured in fixed monthly installments over 1-30 years, depending on the loan type. Borrowers must provide proof of income, a credit report, and asset details. Defaulting on repayments allows the lender to seize the collateral to recover the outstanding amount.

Credit Cards

Credit cards function as unsecured loans with set credit limits and interest rates. While they don’t require collateral, they rely on your credit score, which can suffer if payments aren’t made on time. They’re a quick and flexible alternative but come with higher interest rates than some other options.

Related content: The Differences Between Staking & Crypto Lending

Why Use Ledn for Crypto Loans

Ledn is a comprehensive and user-friendly platform for people looking to leverage their crypto assets without selling them. It offers a range of features designed to provide flexibility, security, and transparency for users seeking crypto-backed loans:

Flexible Loan Options

Ledn provides Bitcoin-backed loans with a loan-to-value (LTV) ratio of 50%, allowing you to access funds without selling your Bitcoin. Loans can be disbursed in USD, USDC, or your local currency, catering to a wide range of financial needs.

Their unique B2X loans combine a Bitcoin-backed loan with the purchase of an equivalent amount of Bitcoin. Upon repayment, borrowers receive both their original collateral and the additional Bitcoin.

You can choose the type of collateral management that works for you:

Standard Bitcoin/ETH-backed loan: Ledn rehypothecates your collateral to lower your interest rates.

Custodied Bitcoin/ETH-backed loan: Collateral is posted to an institutional USD funding partner and held in custody with qualified custodians and banks, ensuring it cannot be rehypothecated.

Read more about Ledn Custodied Loans here.

Quick and Easy

The loan application process is straightforward, with loans funded within 24 hours of receiving the collateral. There are no monthly payments required, and you can repay the loan anytime without penalties, offering flexibility in managing your finances.

Security and Transparency

Ledn is committed to transparency, being the first digital asset lending company to complete a Proof-of-Reserves Attestation. This allows clients to verify that their balances are accounted for in periodic reports, ensuring trust and security. It shares their financial dealings through monthly Open Book Reports.

Partial Loan Repayments

Ledn’s partial repayment feature allows you to make smaller repayments when convenient, without any prepayment penalties. This feature, combined with others like excess collateral redemption and Auto Top-Up, helps optimize your borrowing and holding strategy. Read more.

Global Accessibility

Ledn's crypto-backed loans are available in over 120 countries.

FAQs

What are the risks of crypto loans?

Crypto loan risks are primarily tied to market volatility and platform reliability. If the value of your collateral drops significantly, you may face a margin call, requiring you to provide additional collateral or risk having your assets liquidated. Additionally, choosing an unreliable platform can lead to the loss of your collateral if the lender becomes insolvent. Since crypto lending is less regulated than traditional financial systems, there is also a heightened risk of scams or security breaches. Lastly, failure to repay the loan on time may result in the lender seizing your collateral.

Do crypto loans affect your credit score?

No, most crypto loans do not affect your credit score. Crypto lenders typically do not perform credit checks or report borrowing activity to credit bureaus. Instead, loan approvals are based solely on the value of the collateral provided. This makes crypto loans accessible even to individuals with poor or no credit history.

What happens if the crypto collateral drops in value?

If the value of your crypto collateral falls below a certain threshold, the lender may issue a margin call. This means you must deposit more collateral to maintain the required loan-to-value (LTV) ratio. If you cannot meet this requirement, the lender may liquidate part or all of your collateral to cover the loan.

Are Crypto-Backed Loans Taxed?

The tax treatment of crypto-backed loans depends on your jurisdiction. In many countries, borrowing against crypto is not considered a taxable event, as you are not selling or realising gains on your assets. However, if your collateral is liquidated due to default or margin calls, it may trigger a taxable event, such as capital gains or losses. Consulting a tax professional familiar with cryptocurrency laws in your area is recommended.

Conclusion

Borrowing against cryptocurrency offers a way to access liquidity while retaining your crypto holdings. Platforms like Ledn provide reliable, flexible, and secure loans with unique features such as partial repayments and B2X loans. Get started by opening an account or see how much you could borrow.

Sponsored by 21 Technologies Inc. and its affiliates (“Ledn”). All reviews and opinions expressed are based on my personal views.