Market Commentary

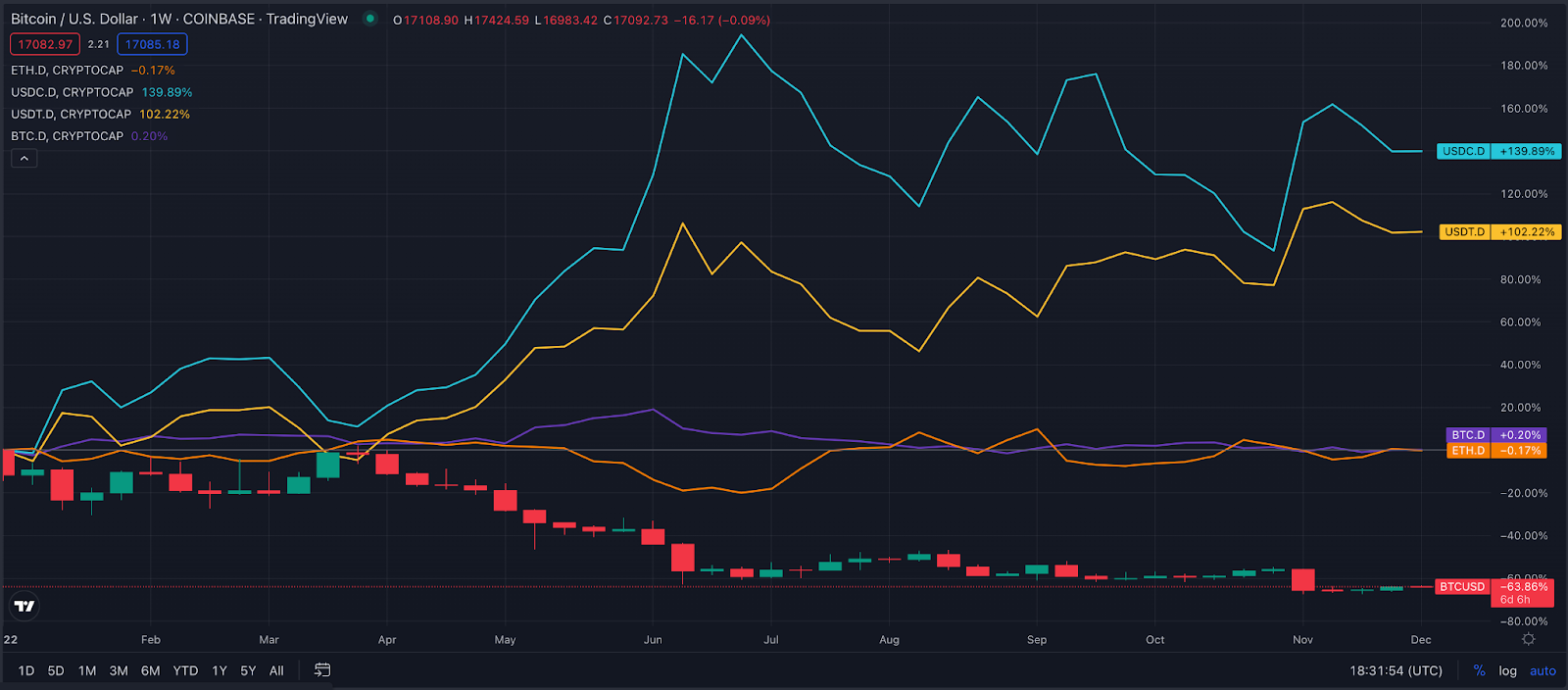

Bitcoin has dropped by approximately -63% year to date, and Ethereum is down roughly -67%. Other crypto assets have experienced even more severe losses. Historically, whenever crypto markets crashed - like in 2018, and 2020, Bitcoin’s share of the total crypto market capitalization would increase. This was seen as the equivalent of the “flight to safety” effect in crypto. Investors would flock to the safest and most liquid asset during times of uncertainty.

However, as you can see from the chart above, this bear market has been different, in that Bitcoin dominance has flatlined near the lows as all crypto asset prices have come under pressure.

So that begs the question - what are investors holding in this environment? The answer is: stablecoins.

At the start of the year, the circulating supply of USDC and Tether stablecoins on Ethereum was $77.83 Billion - today, the same stablecoins account for a circulating supply of 72.38 Billion. That’s a mere 7% drop for the year.

Meaning that, even as the total market capitalization of crypto assets fell by more than 60% from $2 Trillion at the start of the year, to the current ~$815 Billion, the total supply of stablecoins has remained north of $70 Billion. This, in turn, has increased the percentage share of stablecoins relative to the total market capitalization of crypto assets.

The following graph compares the relative market capitalization of Bitcoin, Ethereum, USDC, and USDT vs. the market capitalization of all crypto assets - otherwise defined as “dominance”.

The chart speaks for itself. As is evident from the chart (and the data), stablecoins represent an increasingly growing slice of the total crypto asset pie.

This may confuse North American and European investors. They may ask “but why hold stablecoins, when I can just hold dollars at my bank or put them into a money-market fund?”.

The answer is, most people around the world can’t freely hold U.S. dollars in a place or format that they can trust - nor do they have access to U.S. Treasury bonds. They do not trust their local banks, and saving USD in cash can be a liability in the developing world: it can easily be seized, and there is a big risk of fraud and fake bills. Also to note, U.S cash is not very useful these days as it cannot be used to pay for anything online, nor can it be deposited into a local entity to transact or earn interest.

So, the answer of who is holding these stablecoins is most likely “the rest of the non-U.S. dollar world!”.

The benefits of stablecoins to the developing world are clear as water. Stablecoins can be used in platforms like Ledn, to earn interest or receive loan disbursements. Stablecoins can be easily converted to U.S. dollars or local currency. They are not as volatile as Bitcoin, and increasingly, options are emerging to pay online with stablecoins. Over time, clients will be able to pay with stablecoins anywhere a credit card is accepted. The downside to stablecoins, complexity of use and fees, will likely get eroded or abstracted away in a short period of time.

This is a trend that we expect to continue, as the world, thirsty for dollars, continues to learn about stablecoins. In parallel, companies will continue working on making stablecoins more accessible to the masses. Both trends will converge in a cambrian explosion of solutions that will benefit developing markets in particular.

Sticking with stablecoins, Circle, the operator behind USDC, announced yesterday that it was cancelling its plans to list on the U.S. stock market through its proposed SPAC transaction.

This announcement makes sense given the current market conditions. In simple terms, a SPAC listing is a process whereby a private company that does not trade in the public markets merges with a shell company that trades in the public markets but has no running business.

It’s a process that makes sense when a company in a particularly “hot” sector (like crypto last year), wants to capitalize on investor interest and good market conditions (like last year). For context, Circle announced its plans to list via a SPAC in May of last year - when conditions were much better in both crypto markets and capital markets. Right now, both markets are under a lot of pressure. In the current market context, it makes little sense for Circle - or anyone for that matter, to list via a SPAC.

Another piece of news that flew generally under the radar over the weekend was the fact that Genesis Capital is now negotiating with 2 creditors that total $1.8 Billion in claims.

While not surprising, the news highlights that pressure is building on the Genesis team to come up with a solution for its creditors.

As we mentioned in last week’s dispatch, any resolution on the Genesis Capital case will move markets regardless. A positive outcome - i.e. restructuring debt and reopening withdrawals, would be favourable for prices. Vice versa, a negative outcome should put additional selling pressure on bitcoin and crypto assets in general. Keep an eye for that headline in the coming weeks.

S&P 500

Equity markets soared by more than +3% last Wednesday after Jerome Powell’s speech. During the speech, Mr. Powell provided more clues that the Fed is preparing to raise rates by “just” 50 basis points when it meets next week. The market reaction was confusing to many, including Mohamed El-Erian, who highlighted the communication challenge that the Fed is facing. Any time the Fed as much as hints that it will take its foot off the brakes - regardless of the context it provides, markets rally. Markets rallying makes it much harder for the Fed to meet its inflation targets.

The fact of the matter is that economic conditions are deteriorating, and market reactions to the Fed are driven mostly by “animal spirits”. The “Fed Put” has been programmed into investors’ minds over the years, and it is proving hard to break from it. Based on the reactions to his most recent speech, investors should expect the Fed to accompany its decision to raise by 50 basis points next week with very sobering commentary for markets.

In layman's terms, the Fed is saying “We’re raising interest rates, that should be no cause for celebration”, and the market is responding by saying “Woohoo, let’s ease financial conditions and get this party started again”.

But the data concurs with Mr. Powell, in that there is little to be celebrating in markets at the moment. Here are a few examples:

The chart above shows the deterioration in the U.S. real estate market during previous interest rate hike cycles. As the 2022 line in red shows, the drop in existing single-family home sales during this cycle has been the largest ever - by a long shot.

While average prices have not dropped dramatically - only about 3% from the peak in June, it signals a change in tides. San Francisco, for example, has seen prices fall in the double digits. The fast deterioration has caused some investors to take action, and led to the headline below:

Blackstone, one of the largest asset managers in the world, has paused redemptions, or withdrawals from its $125 Billion U.S. real estate fund. After receiving a surge of redemption requests, the fund has triggered its quarterly redemption limit, and now investors cannot redeem their shares until the next quarter. Effectively, many investors that are long U.S. real estate are running towards the exit door.

As we’ve mentioned in previous dispatches, as long as interest rates are rising, and remain high, markets should remain under pressure as liquidity is drained from the system and into U.S. treasuries.

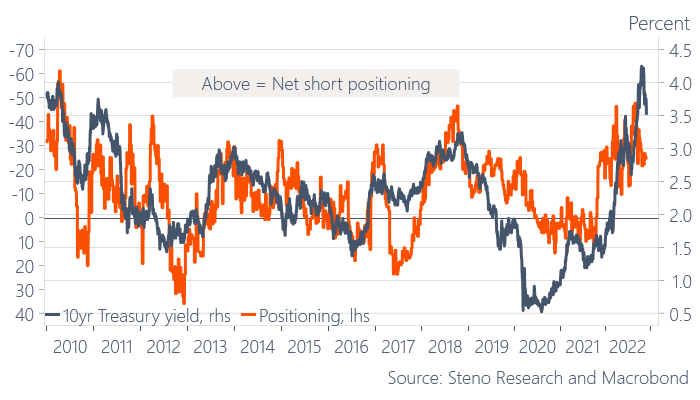

Investor positioning in the U.S. Treasury market, particularly the 10-year bond, is also consistent with this view.

As evidenced from the chart, investors are still net short the 10-year bond. Translation: they are expecting rates to continue rising, therefore dropping the face value of the bond.

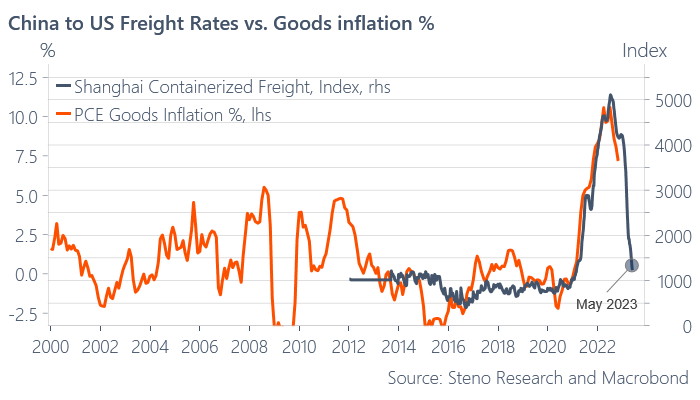

If rates will remain high until inflation is back to the 2-3% range, the important question becomes: “when will inflation be subdued?”. To get some clues, let’s look at the chart below:

U.S. Goods inflation is tightly correlated with the Shanghai Containerized Freight Index. As we can also see from the chart, containers for May 2023 are back within historical prices. This isn’t to say that by May 2023 inflation will no longer be a problem, but it is a good indicator that prices are trending in the right direction that the Fed wants to see. It also marries well with the view that “peak interest rates” will be reached in Q1 2023 - and markets will have one less headwind to deal with for the remainder of the year.

Gold

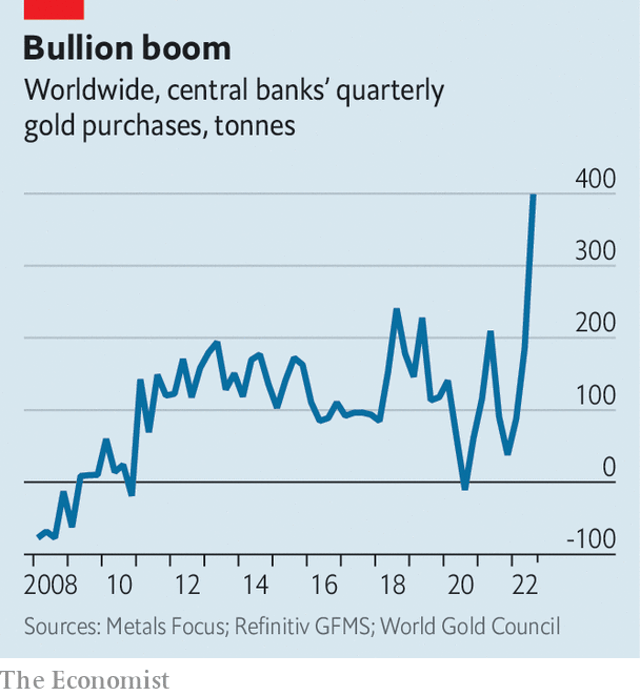

Gold prices have continued hovering north of $1,750/oz. As we’ve flagged in previous dispatches, Central Banks’ appetite for gold has continued making headlines.

The recent article from The Economist echoes what we’ve been writing over the last several weeks. Central Banks are stocking up on gold after they have seen the potential consequences of holding other countries’ debt.

There’s a couple of trends that are fuelling this behaviour: a) gold is “sanction resistant” when compared to U.S. treasuries or other government bonds, and b) the current price offers a compelling risk/reward setup as gold is only down 3% for the year in U.S. dollar terms.

This trend is well poised to continue, especially considering that the Fed is now approaching its stated “peak interest rate”, and inflation is trending to be back at Fed-target levels in a few months. Once interest rates stop rising and inflation comes back into range, gold prices should benefit.

DeFi

It was another relatively quiet week in DeFi land. One of the most relevant headlines was made by Larry Fink, CEO of Blackrock. Mr. Fink said that he believes the next generation of finance will be “tokenized” using blockchain technology.

For context, Blackrock manages about $8 Trillion dollars and signed a deal with Coinbase earlier this year to provide its institutional clients access to bitcoin and crypto assets.

The fact that Mr. Fink is excited about the technology doesn’t mean he is excited about the ecosystem overall. He thinks that most cryptocurrencies as they exist today won’t survive.

Beyond the headlines, Ethereum funds have seen 3 consecutive weeks of outflows, the most recent one seeing $4 Million flow out of funds.

Coinshares analysts suggest that what could be causing the negative sentiment is uncertainty around the ability to “unstake” Ethereum. A key thing to note about the Proof of Stake upgrade is that Ethereum holders can stake Ethereum to earn interest, but they cannot yet “unstake it”, meaning that it is a one-way street right now. However, it could likely be continued de-risking overall as Ethereum did have a significant run-up relative to Bitcoin leading up to the merge.

Difficulty Commentary

The most recent difficulty adjustment, which kicked in last night, dropped mining difficulty by -7.44%. This was a welcome adjustment by the mining community, most of which is operating underwater at the moment.

At current levels, an Antminer S19j Pro, one of the top last-generation machines produced by Bitmain, generates approximately $79/month in revenue - and at the average industrial electricity rate in the U.S., it consumes $82/month in power alone. This means that, even with the current adjustment, most miners in the U.S. are operating well underwater.

Again, it would not be surprising to see consolidation in this space in the weeks and months to come.

The Week Ahead

The week ahead will be relatively light in terms of data and events. There are no Fed speeches this week as members are preparing for their FOMC decision next Wednesday. Prior to next week’s Fed meeting, next Tuesday we will also get the inflation reading for the month of November in the U.S. Expect markets to react to the inflation reading and the interest rate decision announced by the Fed.

Here’s a summary of the events and data that could move markets in the week ahead:

Friday

08.30 AM EST - U.S. Producer Price Index

It's a big week coming up, and as always, we'll keep you posted on any relevant news throughout the week right here and from our Twitter account.

_____________

Notice for U.S. Residents: Effective April 4, 2022, U.S. clients will no longer be able to earn interest on any newly deposited funds in their BTC and/or USDC Savings Accounts, where available; however, they will continue to earn interest on their pre-existing balances in their BTC and/or USDC Legacy Savings Accounts.

This article is intended for general information, educational and discussion purposes only, it is not an offer, inducement or solicitation of any kind, and is not to be relied upon as constituting legal, financial, investment, tax or other professional advice. This article is not directed to, and the information contained herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to law or regulation or prohibited by any reason whatsoever or that would subject Ledn and/or its affiliates to any registration or licensing requirement. This article is expressly not for distribution or dissemination in, and no Ledn product or service is being marketed or offered to residents of, the European Union, the United Kingdom, the United States of America or any jurisdiction in Canada, and such product or service may only be marketed or offered in such jurisdictions pursuant to applicable laws or reliance on regulatory exemptions. A professional advisor should be consulted regarding your specific situation. Digital assets are highly volatile and risky, are not legal tender, and are not backed by the government. The information contained in this publication has been obtained from sources that we believe to be reliable, however we do not represent or warrant that such information is accurate or complete. Past performance and forecasts are not a reliable indicator of future performance. Any opinions or estimates expressed herein are subject to change without notice. This article may contain views or opinions of the author that do not necessarily reflect the opinions, standards or policies of Ledn. We expressly disclaim all liability and all warranties of accuracy, completeness, merchantability or fitness for a particular purpose with respect to this article/communication. Read our Disclaimers at https://ledn.io/legal/disclaimers