Comparison Table

Let’s see what some of the current ETH-backed loan rates are in 2024.

|

Platform |

ETH loan APR |

Loan-to-Value (LTV) |

|

Ledn |

12.40% |

50% |

|

Nexo |

13.90% |

50% |

|

Celsius Network |

X |

X |

|

BlockFi |

X |

X |

|

YouHodler |

8.00% |

50% |

|

CoinRabbit |

12.00% |

50% |

|

SmartFi |

13.00% |

50% |

Updated: April 1, 2024

What is an Ethereum loan?

An Ethereum loan is a loan where you receive a certain currency by using your Ether (ETH) as collateral. You will have to pay the loan back at a clearly defined point in the future, otherwise your collateral will be liquidated.

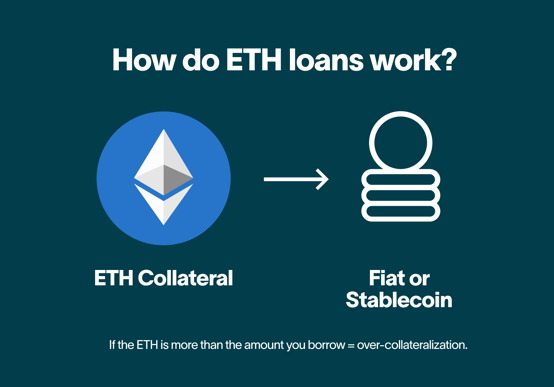

How Do Ethereum Loans Work?

To get an Ethereum loan, you typically must collateralize your ETH, and in return, you are provided with another asset (which is usually fiat or a stablecoin, but it could be another cryptocurrency) for a set period of time. Generally, the amount of digital assets you collateralize for your loan will be more than the amount you can borrow; known as over-collateralization.

The Benefits Of Ethereum Loans

Let’s take a look at some of the benefits that come with ETH-backed loans.

Easy to obtain: Like most cryptocurrencies, it is relatively easy to access an ETH-backed loan. Many services have methods of getting you approved for a loan within a short space of time. For instance, with Ledn, you can secure a loan within 24 hours.

Access fiat without losing your position: One of the most attractive features of an Ethereum loan is that it allows you to obtain fiat for a period without ever trading your ETH for it. This is fantastic if you need fiat, but believe ETH will rise in the short term. It allows you to get the money you need in the form of legal tender, whilst not losing your cryptocurrency in the process.

Capitalize on your Trading Positions: If you are a trader, then you can use Ethereum loans to help strengthen certain positions. For instance, if you own ETH as an investment, but you simultaneously would like to invest in something else via fiat, then you can collateralize your ETH and use the newly borrowed fiat to make a separate investment. However, bear in mind that this contains some inherent and serious risks which you must be mindful of, as a poor investment choice with your borrowed funds could leave you unable to pay your loan, which would lead to your Ethereum getting liquidated.

Ethereum Loan interest rates are typically better than fiat: While this is not always the case, generally speaking, the interest you pay on an Ethereum loan is lower than it is on a typical fiat loan. There are several reasons for this. For starters, crypto lending projects have less overhead costs meaning they can offer better rates. Another factor is that over-collateralization reduces risk on the lender-side, which leads to a reduced need for high rates.

How To Get The Best Ethereum Loan Rates In 2024

Let’s look at some simple methods you should keep in mind for obtaining the best Ethereum loan rates.

Understand your options: Look into the types of loans on the market, and whether they are suitable for you. This means you must evaluate your finances, the amount you want to borrow, and what your aims are in gaining a loan. For instance, two of Ledn’s loan options are Standard and Custodied– both of these work in slightly differing ways, which we will explore later on.

Pick the right platform: It goes without saying that no two lending providers will work in exactly the same way. For this reason, some platforms offer lower interest rates than others. Make sure to look around and be mindful of this, so that you can get the best deal for your needs.

Understand what affects crypto loan rates: Getting a grasp of the fundamentals of crypto and Ethereum loan rates will help you to navigate the space with more ease. For instance, risk, volatility, and supply and demand are just some of the factors at play here.

Do not worry if you are unsure about any of the elements listed, as they will get explored and unpacked here in this guide, which should arm you with the right knowledge to find the best Ethereum loans on the market.

Types of Ethereum Loans Available

There are several types of Ethereum loans on the market. Let’s discuss two of the main ones here.

Custodied Loans: A custodied ETH-backed loan is where your collateralized ETH is held with a qualified custodian or bank, where it cannot be touched, even by the company issuing the loan. If you work with Ledn for this, then your collateral will be posted to an external USD funding institution. The idea is that, when you access a custodied loan, you are given the highest form of peace of mind, as you know that your assets will not be used for a means of the lender generating profits. As a result, your collateral is not subject to any level of counterparty credit risk or rehypothecation risk.

With that being said, this does come with a drawback– you will be paying a higher interest rate. Simply put, the extra cost goes towards the added security, as well as to financially offset the fact that the lender will not engage in any investments or activities with your funds.

Standard Ethereum Loans: When you access a standard Ethereum loan, your collateralized ETH is handed to the lender in question, where you agree to let them use it as a means of earning interest themselves. For instance, with a standard loan, a lender can further choose to lend your ETH out themselves. The upshot is that by doing so, you are provided with a lower interest rate, as the service itself is offsetting any risks incurred by the loan.

Factors That Affect Ethereum Loan Rates

Let’s now assess some of the methods that affect rates for Ethereum loans. Having a gauge of this will help you to make the most informed decisions, as well as simply understand the mechanics and underlying factors that make up the ETH lending space.

Annual Interest Rate (APR): Your annual interest rate, or APR, is the primary factor in determining how much you will be paying for your loan. It is the percentage of interest you will pay, as a yearly figure. That does not necessarily mean you only pay interest after one year, or only if you have a loan open for a year– this is more so the standard method of calculating rates. The APR is made up of many elements, such as volatility in the market, risk associated with lending (for the service itself), and supply and demand.

In the case of custodied loans, the APR will be higher as a means of pricing in the risk that comes with lending to somebody and the lender being unable to rehypothecate the collateral. Standard loans will have a lower APR to reflect the fact that the lender has more control over the collateral, which they can lend out to others and earn additional interest.

However, some aspects will affect APR for all types of Ethereum loans. For instance, if ETH becomes more volatile in the long-run, then the APR could rise for both custodied and standard loans.

Loan-to-Value: Your loan-to-value (or LTV) is the ratio of a loan to the value of the asset being borrowed. The higher the LTV, the more you are borrowing, relative to the asset’s value. A higher LTV will typically incur higher rates, because it represents a greater risk to the lender. When the loan amount approaches or exceeds the value of the collateral securing the loan, there is a higher chance that the lender might not be able to pay it back.

Loan amount: While APR is a major component of calculating cost, it is far from the only aspect to keep in mind. The amount you are seeking is hugely influential. Higher loan amounts may have higher rates to coincide with the risk involved. For example, there is inherently more risk in a project lending out $750,000, compared to it lending out $12,000. And so the rate is reflected by this.

Collateral requirements: In crypto, over-collateralization is the norm. This is where you post more than your loan is actually worth. It is used largely because many crypto services (both CeFi and DeFi) are unable to access your credit history, and so they cannot use it to form a basis of trust. Without this type of data, the best way to mitigate risk is to require users to overcollateralize. The positive is that doing so tends to reduce the APR of your loan, as the risk is considerably dropped. If a service allows you to pay extra for collateral, then doing this could also lower APR, which is beneficial if you would prefer to pay more for the loan upfront than via interest over time.

Loan duration: The length of your Ethereum loan period will affect its rates. Depending on the service you use, a shorter loan duration could lead to higher interest rates, as there is a higher risk of not paying back due to the reduction in time. In a similar sense, you could get a shorter interest rate for borrowing over a longer period of it. However, pay attention to the way that interest accrues depending on the duration. For some loans, interest is added daily, for others it is more dynamic.

Platform fees: There is a cost that comes with running a lending service, which is often passed on to borrowers. Granted, it is almost always lower than with fiat institutions as crypto projects usually do not have physical branches or employ many individuals in comparison. However, they still exist nonetheless.

Credit checks and application process: As mentioned above, many crypto lenders do not conduct credit checks. This is always the case with DeFi projects, however, some CeFi services do not either. This includes Ledn. Rather, the lack of knowledge that comes from avoiding credit checks is often priced into the loan itself, either via its APR, its level of over-collateralization, or other fees. This might be viewed as a negative, but it is good to consider that even with this in mind, crypto loans are often more cost-effective than their fiat counterparts.

Not only this, but for users who (by no fault of their own) have poor credit scores, the fact that services like Ledn take a different approach makes for a more open and welcoming experience. Credit scores may come easy to some, but for many people around the world, they can provide an unfair and improper account of somebody’s life, which locks them away from financial tools. For instance, in countries where fiat is unstable, and access to the US dollar is limited, these individuals are less likely to have a decent credit score. The same is true for those who are unbanked or underbanked, which makes up a sizeable portion of the world.

Even people who have access to a relatively stable legal tender, and who have bank accounts, can still get treated unfairly from a credit score perspective. This could be due to medical complications and bills, identity theft, and issues of cashflow that are not their fault (such as being poorly paid at work). This is not to mention those who simply do not have a credit score at all, which includes people who were never taught economic literacy and believed that owing debt was inherently detrimental, as well as immigrants and asylum seekers who do not have official documentation or records that can be ported over to a credit checking service.

It goes without saying that the credit system is deeply flawed. While you could say that a credit check might potentially allow for a decrease in some loan rates, it is also fair to say that avoiding this route may be ideal for more people. And so long as a project keeps platform fees low and adheres to current market sentiment on crypto lending rates, then they should not be priced harshly.

Conclusion

There are many services out there offering Ethereum loans in 2024, all with different processes, methods, and rates. Now that you have a good idea of how these rates are constructed, and you know what to keep in mind when searching for lending options, it is a great idea to check out some of the top services on the market. Be sure to visit Ledn, and take a look at what their lending options are like, and whether they align with your goals.

Sponsored by 21 Technologies Inc. and its affiliates (“Ledn”). All reviews and opinions expressed are based on my personal views.